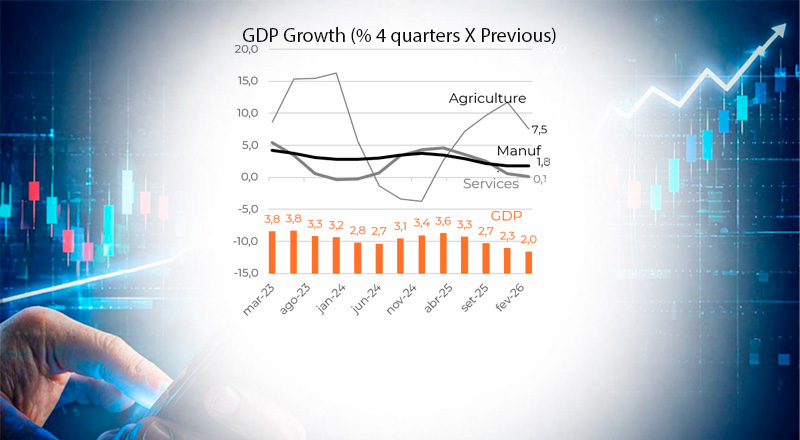

- Brazil’s GDP grew 1.1% in Q1 2026 quarter-over-quarter. Although the result was broadly in line with analysts’ expectations, it is noteworthy given the recovery from the weaker performances recorded in Q2 2025 (+0.34%), Q3 2025 (+0.10%), and Q4 2025 (+0.26%)—an average growth rate of just 0.2% during that period.

- On the production side, sectors linked to external demand stood out positively: agriculture expanded 2.03%, while extractive industries grew 3.64%. By contrast, sectors more sensitive to domestic consumption, such as manufacturing and services, increased by only 0.07% and 0.48%, respectively, both below overall GDP growth. Even so, household consumption rose by a robust 0.96%.

- The strong growth in household consumption, combined with elevated inflation—which is expected to fluctuate near or above the upper limit of the inflation target by the end of 2026—may lead the Central Bank to adopt a more cautious approach to monetary policy. In other words, the risk has increased that the Selic rate will end the year above 13%.

- On the other hand, given expectations of extremely high interest rates and the elevated indebtedness of both households and the government, it is unlikely that the pace of consumption seen in Q1 2026 will be sustained. This is especially true if the labor market continues to lose momentum. In that context, would inflation reflect this moderation in demand and allow for the continuation of a gradual recalibration of interest rates? Potential declines in oil and fuel prices could also help. Worth monitoring.

- On the economic calendar, the main domestic highlight will be Brazil’s April 2026 industrial production data. In the United States, attention will focus on the May 2026 labor market report.

HIGHLIGHTS (WORLD/BRAZIL): from May 25 – 29

GEOPOLITICS

Nvidia announced plans to invest US$150 billion per year in Taiwan. The announcement was made during the launch of the company’s new headquarters project in the country, which is expected to be operational by 2030. The initiative is expected to strengthen Nvidia’s relationship with TSMC, the world’s leading contract chip manufacturer.

China threatened to retaliate against potential trade restrictions currently under consideration by the European Union. The EU has discussed measures such as expanding the use of tariffs and import quotas to curb the inflow of products subsidized by foreign governments.

INTERNATIONAL ECONOMY

Despite the acceleration in U.S. 12-month inflation as measured by the PCE—from 3.5% to 3.8% between March and April 2026—some analysts believe that a degree of disinflation may emerge in the coming months. This view is supported by the core inflation reading, which rose only 0.2% month-over-month, the lowest monthly increase of the year.

China’s outbound investment totaled US$62.9 billion from January to April 2026 (+3.9% year-over-year). Excluding stock market investments, outbound investment amounted to US$46.4 billion (-13.9% year-over-year), spread across 5,231 companies in 142 countries and regions.

BRAZILIAN POLITICS

The Chamber of Deputies approved Bill 699/2023, which creates Profert, an incentive program for the fertilizer industry. The program grants tax credits between 2027 and 2031, with an annual cap of R$2 billion and a cumulative limit of R$10 billion over the period.

Populist measures with fiscal impacts announced by the federal government in 2026 (through May) amount to R$184.7 billion. In 2022 (through May), announced measures totaled R$74.5 billion (at April 2026 prices).

BRAZILIAN ECONOMY

GDP grew 1.1% quarter-over-quarter in Q1 2026, recovering after an average quarterly growth rate of just 0.2% between Q2 2025 and Q4 2025. Agriculture and extractive industries were the main highlights, expanding 2.0% and 3.6%, respectively. Household consumption accelerated from an average of 0.25% in Q2–Q4 2025 to 0.96% in Q1 2026.

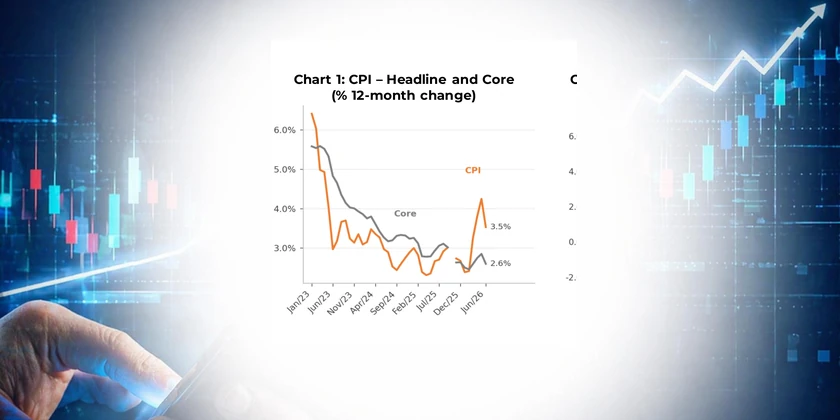

The IPCA-15 rose 0.62% in May 2026, exceeding expectations of a 0.57% increase. The result reflected higher prices for food, electricity, and personal health care, which together accounted for 85.5% of the month’s inflation. Twelve-month inflation increased from 4.37% to 4.64%.

EQUITIES AND COMMODITIES: from May 25 – 29

MARKETS I: EQUITIES AND COMMODITIES (from 04/27/2026 to 04/30/2026)

- The S&P 500 extended its winning streak to nine consecutive weeks and reached a new high for the year, rising 1.43% during the week and 5.15% over the month. The Nasdaq also posted a new yearly high, advancing 2.89% during the week and 10.49% over the month, supported by continued strength in technology stocks.

- Lower oil prices and easing interest rates boosted other equity markets. The Nikkei gained 4.72% during the week and 11.88% over the month.

- The Ibovespa fell 1.37% during the week, marking its seventh consecutive weekly decline, ending at 173,787 points. The index is now 12.5% below its all-time high of 198,657 points, reached on April 14.

- Net foreign inflows into B3 totaled R$42.4 billion over the first 99 trading days of the year, substantially above the R$20.9 billion recorded during the same period in 2025. However, this figure remains below the R$69.1 billion recorded on April 14.

- Between April 15 and May 27 (29 trading days), foreign investors recorded a positive net balance between purchases and sales of equities on B3 on only two trading days. Over the period, R$26.6 billion in foreign capital left the Brazilian stock market.

- The price of the Brent crude oil futures contract fell 11.10% during the week, closing at US$92.05 on May 29, while WTI crude oil declined 9.57%, ending at US$87.36.

- As a result, year-to-date gains through May 29 stood at 51.27% for Brent and 52.14% for WTI, down from 70.16% and 68.23%, respectively, one week earlier.

- The price of natural gas (Dutch TTF) fell 5.51% during the week, though it still posted a 63.35% gain year-to-date as of May 29.

- Gold rose 0.68% during the week to US$4,540 per troy ounce, while silver declined 0.32% to US$75.30.

- Industrial commodity prices generally increased during the week, with aluminum up 0.47% and nickel up 0.79%. Copper, however, declined 0.23% over the same period.

MARKETS II: CURRENCIES AND INTEREST RATES

- Yields on 10-year U.S. Treasury securities declined from 4.56% to 4.44% between May 22 and May 29, after reaching 4.67% on May 19, their highest level of 2026. Lower oil prices have eased part of the inflationary pressure, contributing to a decline in long-term interest rates despite ongoing fiscal concerns.

- In Brazil, the interest rate curve remained relatively stable. An IPCA-15 reading above expectations and a resilient economy have increased the challenge facing the Central Bank, overshadowing the positive effects of lower oil prices. With gross public debt reaching 80.4% of GDP in April 2026, the highest level since June 2021, the fiscal outlook continues to deteriorate. The January 2029 DI contract edged down from 13.85% to 13.84% between May 22 and May 29.

- In the May 22 Focus Survey, expectations for IPCA inflation at the end of 2026 rose to 5.04%, moving further away from the upper limit of the inflation target range. At the end of February 2026, the corresponding expectation stood at 3.91%.

- Expectations for IPCA inflation at the end of 2027 were 4.01%, compared with 3.79% at the end of February 2026.

- The DXY U.S. Dollar Index weakened during the week, supported by lower oil prices and easing pressures in interest-rate markets. Among the index’s major currencies, the euro (EUR) appreciated 0.48%, while the British pound (GBP) gained 0.17%. The Japanese yen (JPY) depreciated a modest 0.06%, with losses limited by intervention from the Bank of Japan.

- The Brazilian real (BRL) remained at R$5.04 per U.S. dollar, representing a 1.62% depreciation over the month. Despite this, the real remains among the best-performing currencies of the year, with an appreciation of 8% year-to-date.

- The 21-day moving average of Brazil’s foreign exchange flow stood at US$10.4 billion as of May 22. Between May 15 and May 22, the commercial flow moving average increased from US$10.8 billion to US$11.1 billion, while the financial flow moving average declined from US$2.2 billion to negative US$0.7 billion.

·

SECTORS AND REGIONS

WORKWEEK REDUCTION CONSTITUTIONAL AMENDMENT

▪ The Chamber of Deputies approved, in two rounds of voting, a constitutional amendment that will reduce the standard workweek from 44 hours to 40 hours, to be implemented within 14 months of promulgation. The proposal has now been forwarded to the Senate for review and voting.

▪ The Senate has also introduced Constitutional Amendment Proposal (PEC) 12/2026, which establishes more flexible rules for reducing weekly working hours, allowing for individual agreements and compensation adjusted to hours worked.

AGRIBUSINESS

▪ Camex approved anti-dumping measures on powdered milk imported from Mercosur countries, although implementation will depend on an assessment of the potential inflationary impacts. The investigation, launched in 2024, identified dumping margins exceeding 60% on powdered milk imported from Argentina and Uruguay.

▪ The risk of an El Niño event developing in the second half of 2026 could delay soybean planting and shorten the planting window for the second corn crop, particularly in the Matopiba region and Brazil’s Center-West.

FUELS

▪ Brazil’s National Agency of Petroleum, Natural Gas and Biofuels (ANP) postponed its decision on launching a public consultation regarding new rules governing access to natural gas pipelines and gas processing facilities. Estimates suggest these measures could reduce industrial natural gas prices by as much as 52%.

▪ The federal government published a decree granting a R$0.44 per liter subsidy on gasoline. In addition, it issued a regulation establishing a R$0.35 per liter subsidy on diesel fuel, effective June 1, and extended through July 31 the reduction in PIS/Cofins taxes on aviation kerosene.

INDUSTRY

▪ According to a survey conducted by the National Confederation of Industry (CNI), the illicit market causes annual losses of approximately R$107 billion. The main impacts identified include lost gross revenue, reduced market share, and higher security-related costs.

▪ According to data from Anfavea for the first four months of the year, the share of plug-in hybrid and fully electric vehicles in total electrified vehicle sales increased from 40.5% in 2022 to 65.4% in 2026. Over the same period, the share of conventional hybrids declined from 59.5% to 34.5%.

CONSUMER BEHAVIOR

▪ Brazilian consumers are reducing their average purchase ticket size while increasing shopping frequency, according to a survey by Elo Insights. Potential drivers include social media, online sales channels, and the growing presence of micro-stores.

▪ Part of the decline in average ticket size and increase in shopping frequency may reflect tighter household budget constraints. A survey by NielsenIQ found that supermarket sales targeting higher-income consumers grew 4% in Q1 2026, while sales at stores serving lower-income consumers declined 9%.

TELECOMMUNICATIONS

▪ Anatel launched a public consultation process to gather suggestions regarding the regulation of Brazil’s submarine telecommunications cables. The consultation period will remain open for 45 days starting May 26.

▪ Currently, submarine cable landing points are heavily concentrated along Brazil’s coastline—particularly in Fortaleza, Rio de Janeiro, Praia Grande, and Santos—and the agency sees this concentration as a potential vulnerability to the country’s telecommunications connectivity.