Bottom Line. The May IPCA report suggests that the disinflation process observed in the second half of 2025 has come to an end. Inflation rose by 0.58% month-over-month and 4.72% year-over-year. While the data do not warrant a renewed tightening cycle, they do shift the focus of monetary policy toward preserving the credibility of Brazil’s inflation-targeting regime and preventing a further deterioration in inflation expectations.

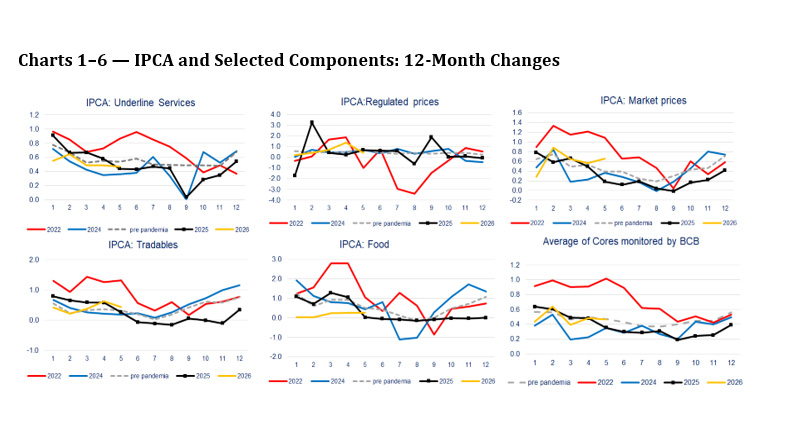

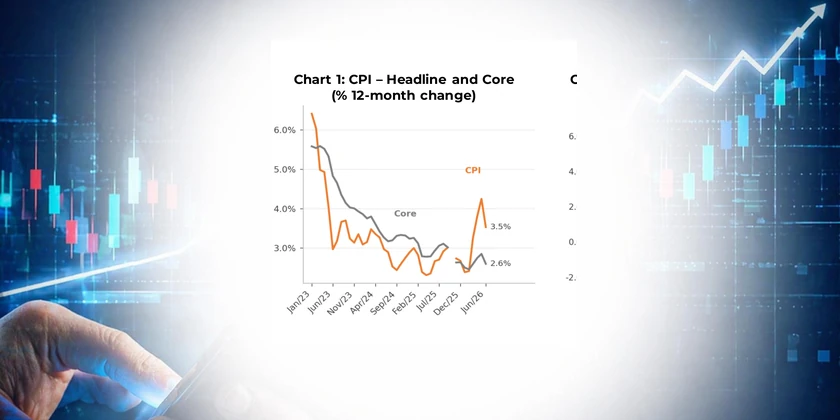

Despite the recent setback, inflation dynamics in 2026 remain considerably less severe than those observed in 2022. During the first five months of the year, food prices, core services, tradable goods, and the core inflation measures monitored by the Central Bank have all posted significantly lower increases than those recorded during the period marked by the war in Ukraine, the surge in oil and commodity prices, climate-related shocks, and post-pandemic stimulus measures. (Charts 1-6)

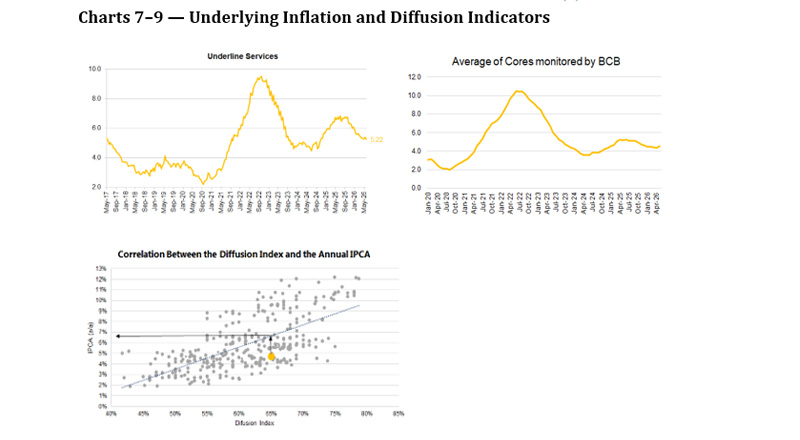

Underlying inflation also remains relatively contained. Core services inflation stands near 5.2%, the average of the Central Bank’s core measures remains close to 4.4%, and the diffusion index hovers around 65%, a level historically consistent with inflation in the 5%–7% range. (Charts 7- 9)

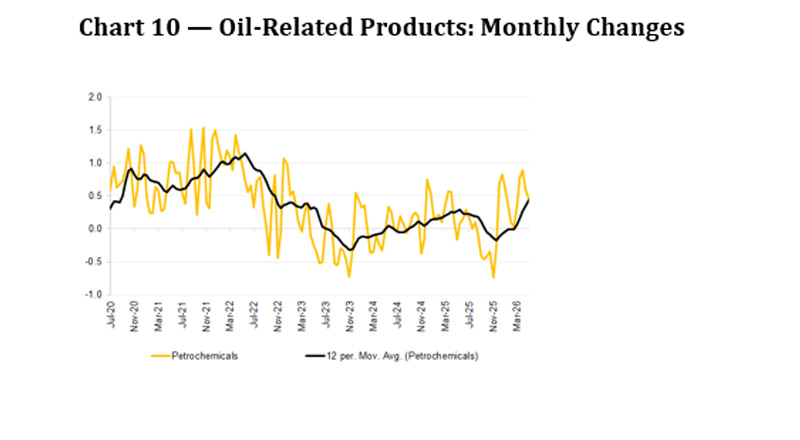

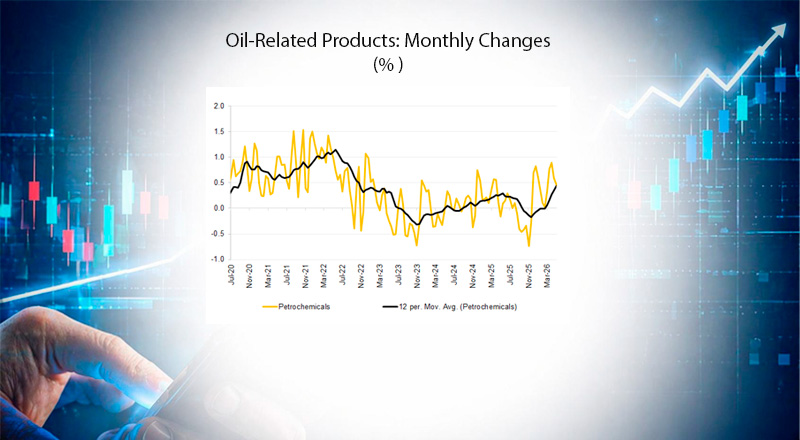

The comparison with 2025, however, is less reassuring. Despite the appreciation of the Brazilian real, the main components of the IPCA have evolved broadly in line with last year’s pattern, suggesting that the oil shock has already offset a meaningful portion of the disinflationary impulse stemming from the exchange rate. With upside risks still concentrated in items exposed to energy prices, a disinflation path similar to that observed in the second half of 2025 now appears unlikely. (Chart 10)

In this environment, the Central Bank’s reaction function is likely to remain focused on preserving confidence in inflation convergence. The de-anchoring of expectations raises the cost of disinflation by increasing inflation inertia. Although ex-ante real interest rates remain between 9% and 10%, well above the estimated neutral rate of around 5%, the room for monetary easing remains limited.

www.linkedin.com/in/tatianapinheiro