| – We have repeatedly drawn attention to the inconsistency of the current macroeconomic approach: aggressively expansionary fiscal and quasi-fiscal policies requiring monetary tightening. In the following pages, we argue that the current policy mix has significantly intensified wealth inequality in the country, despite its redistributive disguise. – According to our estimates, indebted households alone paid approximately R$ 770 billion in interest in 2025 (net of defaults). A large portion of these resources went to the government (around R$ 126 billion), bank profits (approximately R$ 134 billion), and savers (roughly R$ 250 billion). The remainder (R$ 260 billion) were lost through costs and inflation. – Naturally, the benefit to rentiers is not limited to the estimated R$ 250 billion. This is merely the component extracted directly from indebted individuals. The total gain is far greater when one considers the massive transfers originating from corporations and the public sector (by far the largest debtor). This is the consequence of the current economic policy mix: a massive transfer of wealth. |

Introduction

The contrasts within the Brazilian economy appear to have intensified in recent years. On one hand, we observe strong growth in the wage bill alongside historically low unemployment rates. On the other, we witness a debt-fueled expansion among households and the public sector amid extraordinarily high interest rates.

We have repeatedly highlighted the inconsistency of the current macroeconomic framework: aggressively expansionary fiscal and quasi-fiscal policies requiring tighter monetary conditions. See Public Spending Rises 30% Above Inflation in 6 Years, Government Concerned About the Debt… of Others! and Fiscal and Credit Activism Working Against the Central Bank and in Favor of Debt Expansion. In the following pages, we argue that the current approach has significantly worsened wealth inequality in the country, despite its redistributive rhetoric.

The Average is a Dangerous Simplification

National accounts calculate net interest received by households as property income. From an accounting and aggregate perspective, income earned on financial assets is netted against interest paid on debt to derive the net gain of the representative individual.

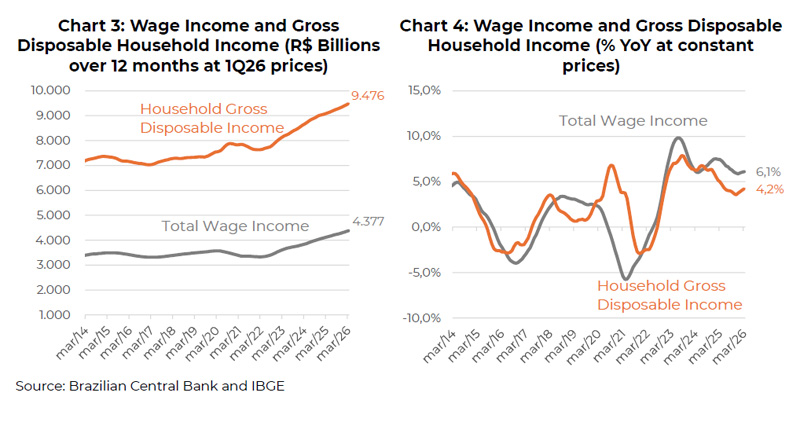

It is therefore tempting to evaluate the average population’s well-being solely through the lens of income dynamics, or at most by considering the net impact of interest payments. The following charts display total labor income and gross disposable household income (which includes the interest account), both at constant prices from the first quarter of 2026. Indeed, how could one fail to be satisfied with annual gains in wages and income, above inflation, of around 5% per year in recent years?

A methodological clarification regarding the previously presented data is necessary. Gross Disposable National Income of Households (RNDBF) corresponds to total income, including earnings derived from production factors (labor and capital), plus transfers received net of transfers paid, such as taxes and social contributions.

This measure represents aggregate household income available for final consumption and savings. More specifically, RNDBF includes the following household income components: labor compensation, including employee wages and gross mixed income; gross operating surplus, mainly corresponding to rental income; property income, including net interest received, distributed corporate income, and investment income, minus income paid for the use of natural resources; and social benefits, including social security benefits and other forms of social assistance.

From this total, transfers paid by households to other institutional sectors and abroad are deducted: income and wealth taxes; effective household social contributions; and other net current transfers made by households.

Debtors Transfer Income

If one evaluates social welfare exclusively through the evolution of average income, one could conclude that higher interest rates would always be desirable whenever the stock of fixed-income assets exceeds household indebtedness. But this is clearly not true.

First, because the aggregate benefit of interest income for households represents a burden for corporations and government, which are predominantly net debtors. The negative impacts on productivity and investment decisions are obvious.

But there is also a second factor of extreme importance: the level of interest rates influences the magnitude of income transfers between debtors and creditors within the household sector itself. In this sense, averages may conceal a great deal.

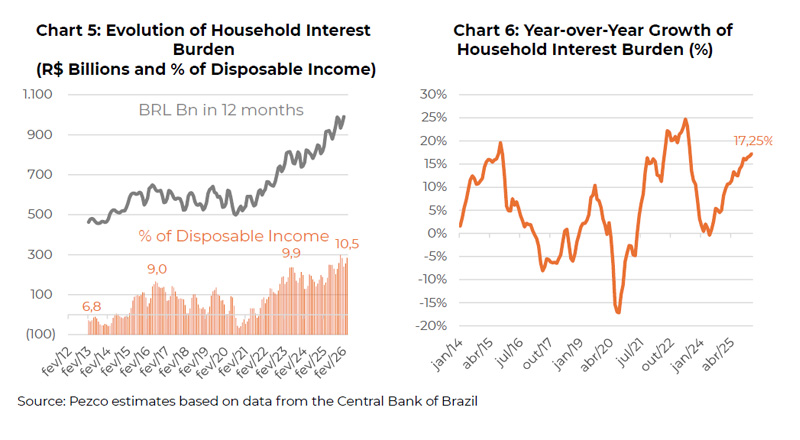

The following charts show the evolution of interest expenses on household debt. While real income has risen 25% in real terms since 2020, debt servicing costs have increased 74% over the same period, from

R$ 536 billion to R$ 930 billion annually.

The comparison between the growth in financial burdens and labor income is even more striking. While the wage bill increased by R$ 745 billion per year during the current decade, the interest burden rose by R$ 395 billion. In other words, almost 50% of the additional resources generated through paid professional activities were directed toward servicing debt-related charges.

Destination of Debtors Income

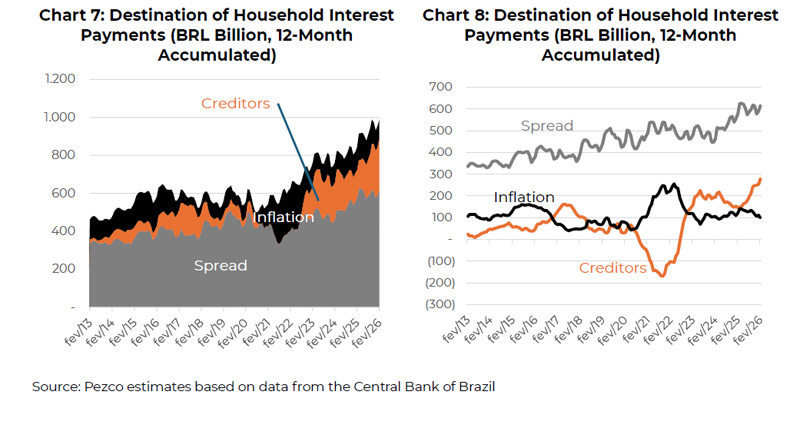

The Central Bank of Brazil publishes statistics regarding the share of disposable income committed to interest payments by households. The monetary authority also releases, on a monthly basis, information on nominal interest rates and spreads associated with credit granted by the financial system to households. Based on these data, it is possible to estimate how much of the amount spent on interest payments by Brazilian households is appropriated by financial institutions (thorough banking spreads), how much is transferred as income to bank investors and depositors, and how much is lost through the inflationary process. Charts 7 and 8 illustrate this dynamic over the past 12 years.

As previously discussed, the interest bill increased from approximately R$ 536 billion before Covid (2019) to

R$ 932 billion in 2025. Of this increase (a total of R$ 396 billion), R$ 66 billion would have been captured through higher spreads, R$ 24 billion lost through the inflationary process, and R$ 220 billion absorbed by investors and bank depositors.

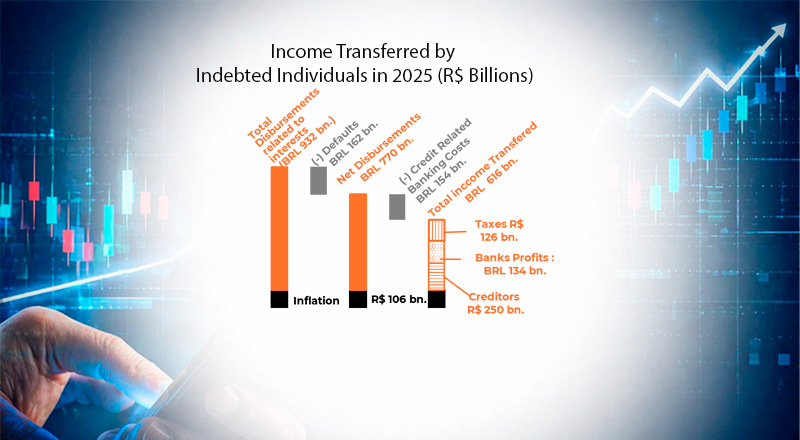

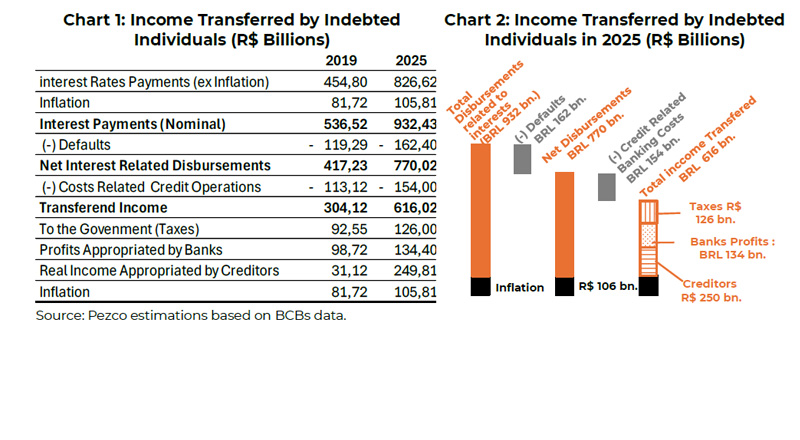

It is possible to go even further. Based on the latest Banking Economics Report published by the Brazilian monetary authority, we decomposed the portion attributed to banking spreads into defaults (amounts not paid by debtors, which must be deducted), banks’ administrative expenses, financial institutions’ profits, and taxes paid to the government. The results of this estimate are illustrated in Charts 1 and 2 on the first page.

According to our estimates, indebted households alone paid approximately R$ 770billion in interest in 2025 (already net of defaults). Of this total, around R$ 154 billion may have been absorbed by financial institutions’ administrative costs and inflation. The transfer of income from debtors may have benefited the government (R$ 126 billion), bank profits (R$ 134 billion), and savers (R$ 250 billion).

Naturally, the benefit to rentiers is not limited to the estimated R$ 250 billion. This is merely the component extracted directly from indebted individuals. The total gain becomes far larger once one considers the massive transfers originating from corporations and the public sector — by far the largest debtor. This is the consequence of the current economic policy mix: a gigantic transfer of wealth.