Summary and Conclusions

| It is misleading to attribute to advocates of fiscal adjustment the intention of cutting public spending. The pace of expenditure growth in recent years has been so accelerated that simply reducing the speed of expansion would already represent a remarkable improvement. “Containing” seems to be a more appropriate verb. Among the various benefits of a less wasteful state, the possibility of enabling lower interest rates stands out. If current budget projections materialize, Brazil is on track to conclude the first six years of the decade (2022–2026) with expenditure growth approximately 29% above inflation (an average of 4.3% per year). This implies a doubling of real spending every 15 years. |

Much has been said about the need for the government to reduce spending to achieve a fiscal result consistent with debt sustainability. The most optimistic estimates point to the need for a primary surplus (revenues minus expenditures excluding financial accounts) of around 1% of GDP, based on the assumption that the real interest rate could stabilize at roughly 1.3 percentage points above GDP growth (for example, a real interest rate of 4% alongside GDP growth of 2.7%). More realistic analysts believe that 2% of GDP would be more appropriate, given the combination of real interest rates (4.5% per year) and economic growth (2.2%) observed on average over the past 20 years. The fact is that Brazil remains far from achieving the necessary fiscal balance. The government’s rather unambitious target is 0% of GDP, which, given the usual flexibility in interpretation, tends to become an acceptable political objective closer to -0.7% of GDP. Moreover, the expected combination of interest rates and growth for 2026 appears highly unfavorable.

The data show that public spending has been growing at such an accelerated pace that it is inappropriate to speak of cuts. A highly feasible objective would simply be to reduce the speed of expansion from the excessive rates observed recently. See the charts in previous page.

Accelerated Pace

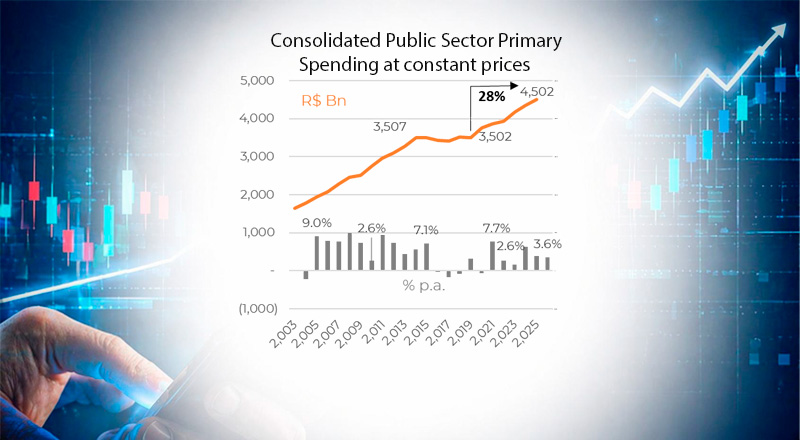

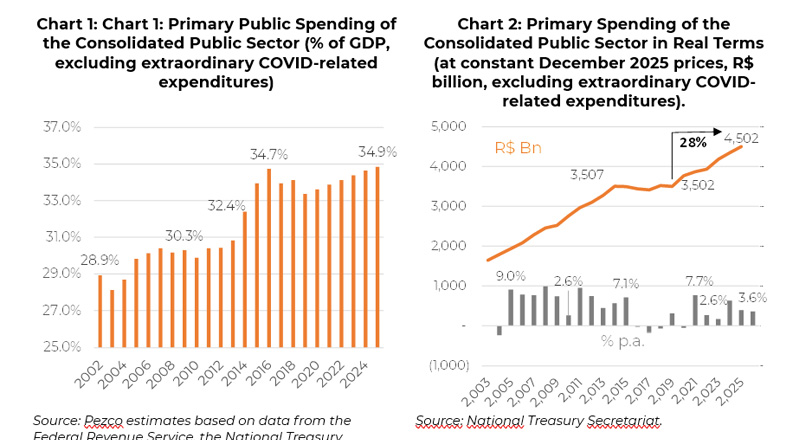

Chart 1 on the previous page presents an estimate of annual primary spending as a percentage of GDP for the consolidated public sector. This figure is not published directly by either the Ministry of Finance or the Central Bank of Brazil. It consists of an estimate derived from subtracting the primary surplus calculated by the monetary authority from the total tax burden. The figure on the right (Chart 2) shows the evolution of total expenditures at constant prices, that is, adjusted for inflation. In both cases, the dynamics observed in the early years of both the previous and current decades are striking. The data also illustrate the effectiveness of the mechanism known as the “spending cap,” introduced in 2017 and abandoned in 2023.

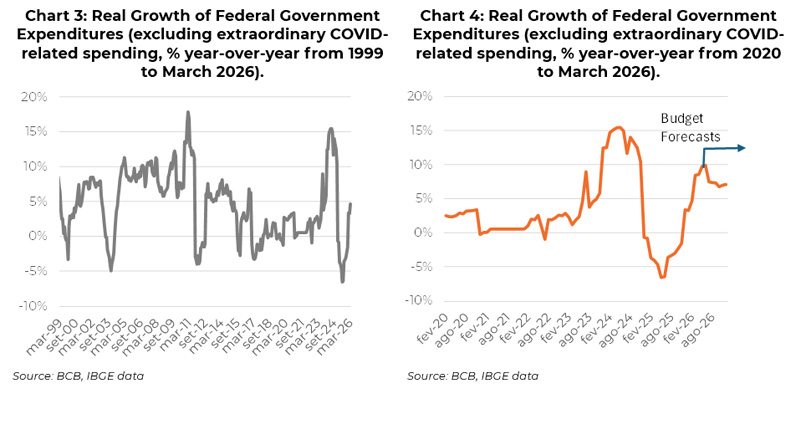

A joint assessment shows that periods of real spending contraction are extremely rare. In practice, cases where expenditure growth approached zero did not result from structural spending cuts. They were either the consequence of inflation surprises or the disappearance of extraordinary expenditures that had occurred in the previous period. This was the case, for example, with court-ordered debt payments (“precatórios”), which inflated the figures in 2023 and 2024, while their absence on the same scale in 2025 produced apparently benign statistics in recent months (see Charts 3 and 4 below).

The conclusion that the recent movement reflects more of a temporary statistical adjustment than an effective austerity policy is reinforced by the government’s own projections, which are usually underestimated and, even in an election period, point to a resumption of spending growth at a pace not far from 5% above inflation (which would imply almost 10% nominal growth) (Chart 4).

If current budget projections are confirmed, Brazil is on track to conclude the first six years of the decade (2019–2026) with expenditure growth approximately 28.5% above inflation (an average of 4.3% per year).

Fiscal Stimulus, Inflation, and Interest Rates

Among the countless benefits of a less wasteful state, the possibility of enabling lower interest rates stands out. Excessive spending expansion has an important side effect in distributive terms: it helps generate inflation (which affects more intensely the portion of the population with fewer tools to protect itself against rising prices) and requires higher interest rates (which aggravates income concentration).

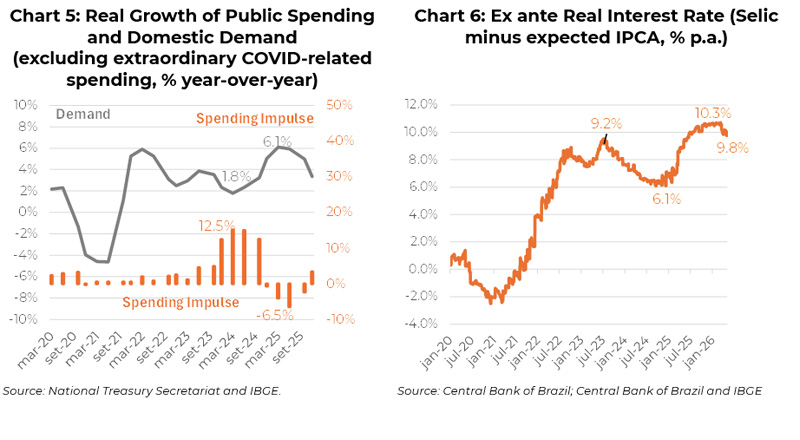

Chart 5 below illustrates how the stronger expansion in demand observed between 2024 and 2025 may have been caused or reinforced by a strongly expansionary fiscal policy. On the right-hand side (Chart 6), we see the monetary authority’s response. The interest-rate cutting cycle that had been underway since 2023 had to be interrupted and replaced by a significant tightening cycle.

In other words, the spending spree observed in recent years contributed to pushing year-over-year inflation from 3.2% in June 2023 to 5.4% in the same month of 2025. The forced march of direct fiscal stimulus combined with increased credit supply from public banks to generate pressure on domestic demand, forcing the Central Bank of Brazil to tighten monetary policy to offset the expansionary impulse. The downward trend in the benchmark interest rate observed since mid-2023 had to be reversed the following year, producing a cycle that raised the Selic rate from 10.5% per year to 15% per year.

The real interest rate measured as the nominal rate minus inflation expectations still stands close to 10% per year. Debt service costs for the consolidated public sector over the 12 months ending last March reached more than 2 trillion reais.

Conclusion

It is misleading to attribute to advocates of fiscal adjustment the intention of cutting public spending. The pace of expenditure growth in recent years has been so strong that simply reducing the speed of expansion would already represent a remarkable improvement. “Containing” seems to be a more appropriate verb. Expansionary fiscal policy generates inflation and higher interest rates. It is even possible to observe a loss of momentum in the fiscal impulse after the excesses of 2023 and 2024. This helps explain the ongoing slowdown in economic activity and could support the monetary authority in deepening the monetary easing process. But then came the war…