- Consumer inflation over the 12 months through last April reached 3.8% in the United States, rising from 3.3% in March and 2.7% one year earlier. The increase was largely driven by higher fuel prices. So far, nothing new.

- What surprised the market was the acceleration in the main core measure, that is, excluding food and energy items. The 2.8% increase (relative to April 2025) came in above expectations of 2.7%.

- The picture points to broader-based price increases than a significant portion of the market had anticipated, reducing hopes that the oil price shock would affect only the set of goods and services more directly dependent on the commodity (the so-called first-round effects). Expectations for interest rate cuts in 2026 are fading away.

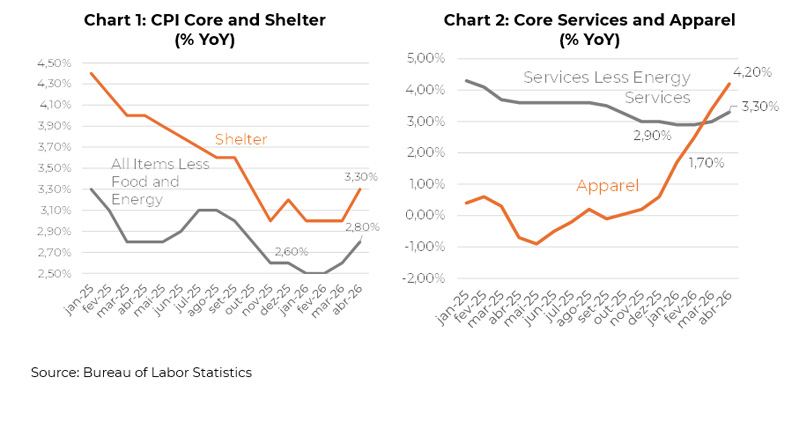

- The fact is that only those who were not paying attention were surprised. We have been highlighting inflationary pressures that have already been evident since late last year, but which had been masked by disinflation in Housing, itself largely driven by methodological factors (as discussed in: US: CPI and PCE Deflator Indicators Pointing in Opposite Directions). See Chart 1.

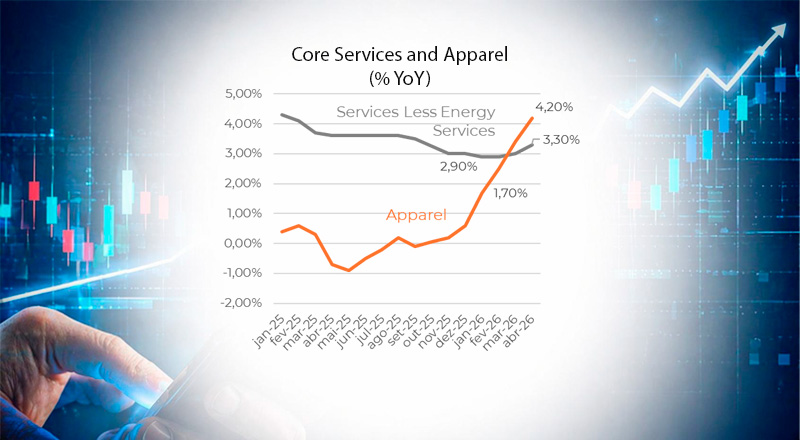

- As early as the beginning of this year, it was also possible to observe the resilience of core services inflation, which was likely to persist under the current environment characterized by accelerating wages (see US – It Will Be Difficult for the Fed to Cut Rates in 2026 and US – Unit Labor Costs and Import Prices: All Roads Lead to Inflation). This is without even considering the pressures in sectors affected by tariff increases, which have also been emerging since late last year (Chart 2).