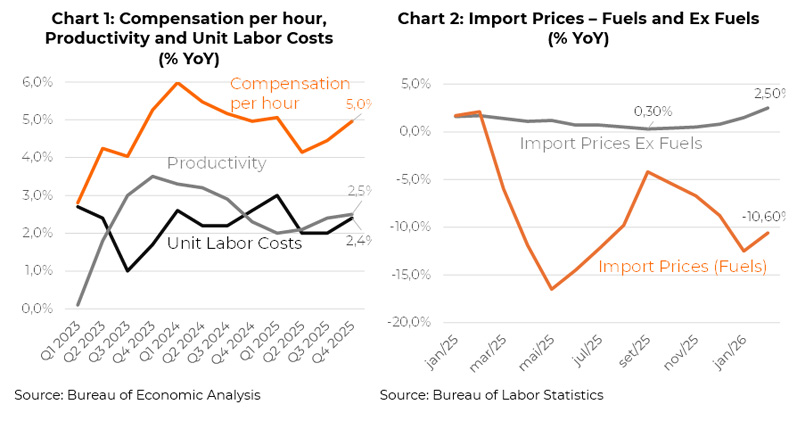

- The monetary authority reduced interest rates last year in response to only a moderate increase in unemployment, but in an environment where the labor market remained tight. Labor supply may face additional constraints due to the aggressive immigration enforcement policy. The fact is that unit labor costs increased 2.4% over the 12 months through the last quarter of 2025, reflecting wages rising 5% and productivity growing 2.2% (Chart 1).

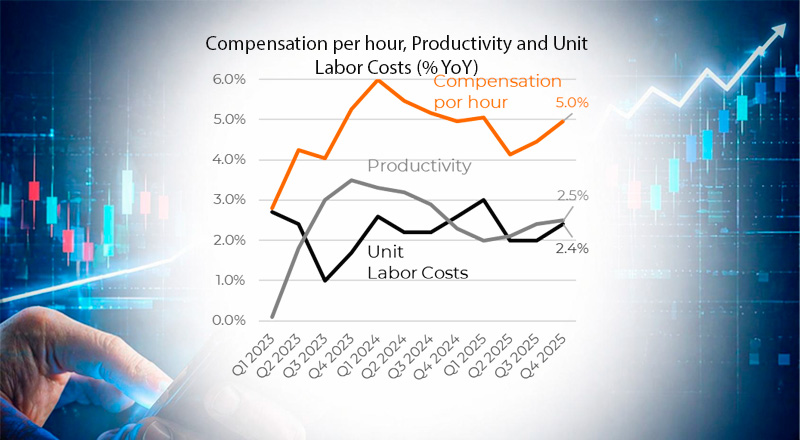

- Meanwhile, the pace of growth in import prices has accelerated since mid-2025, despite deflation in fuel prices and goods imported from China. This is clearly related to higher import tariffs and the depreciation of the dollar in international markets.

- This is particularly relevant because the indicators do not yet incorporate the oil shock.

- Import prices rose 1.3% over the 12 months through February 2026, compared to a 0.3% increase in the same period up to the previous month. The outlook points to further acceleration relative to the negative readings that prevailed throughout 2025. Firms, which had front-loaded purchases earlier in the year to mitigate the tariff shock, are now accepting higher costs and beginning to pass them through to consumers (as reflected in wholesale price indices). Chart 2 illustrates the rising cost of imports, broken down between fuels and other goods.

- As for the labor market, unit labor costs continue to fluctuate between 2% and 2.5% per year, with a greater tendency to accelerate than to ease—something that is not fully consistent with inflation converging to the monetary authority’s target.