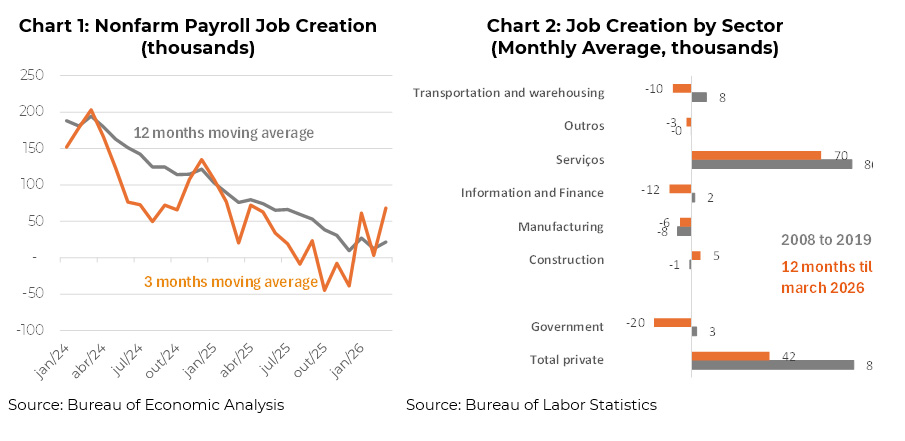

- The payroll data came in reasonably strong in March, corroborating the view that job creation is returning to more normal levels. Nonfarm payrolls increased by 178k and the unemployment rate remained stable at 4.3%. The Gulf war, now lasting over a month, is likely to generate inflation and slow the pace of economic growth. Chart 1 shows that the worst is already behind us on a 12-month cumulative basis, while recent monthly readings appear significantly more benign.

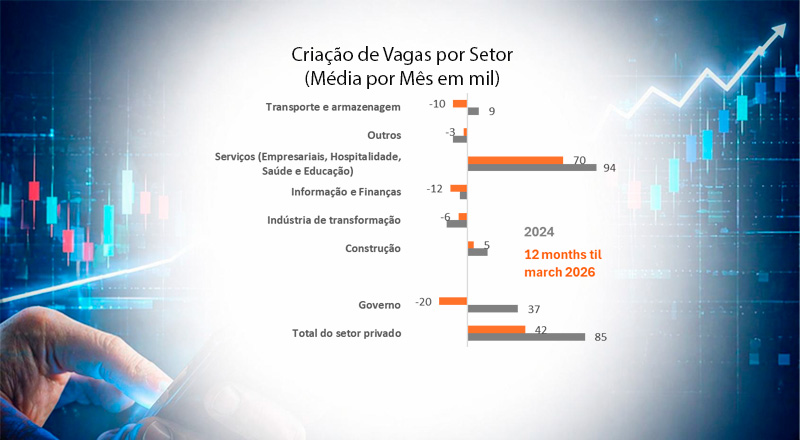

- The lion’s share of the labor market deterioration observed throughout 2025 was associated with job losses in the public sector. The monthly average of 3k jobs added in the recent past (+37k in 2024 alone) shifted to a contraction of 20k jobs on the same basis when considering the last 12 months (see Chart 2).

- The recent recovery in job creation has been more pronounced in the most dynamic segment of the economy, including professional and business services, hospitality, leisure, education, and healthcare. Other sectors such as manufacturing and construction have continued to show stability in employment levels.

- Considering a labor force of around 170 million people, growing at an average pace of 1% per year, we estimate that job creation of approximately 140k per month in the nonfarm sector would be sufficient to maintain equilibrium in the labor market.

- The latest data reinforced the message from members of the Monetary Policy Committee regarding caution on the need for rate cuts. The oil shock and its first- and second-round effects on prices are likely to become increasingly central to monetary policy discussions.