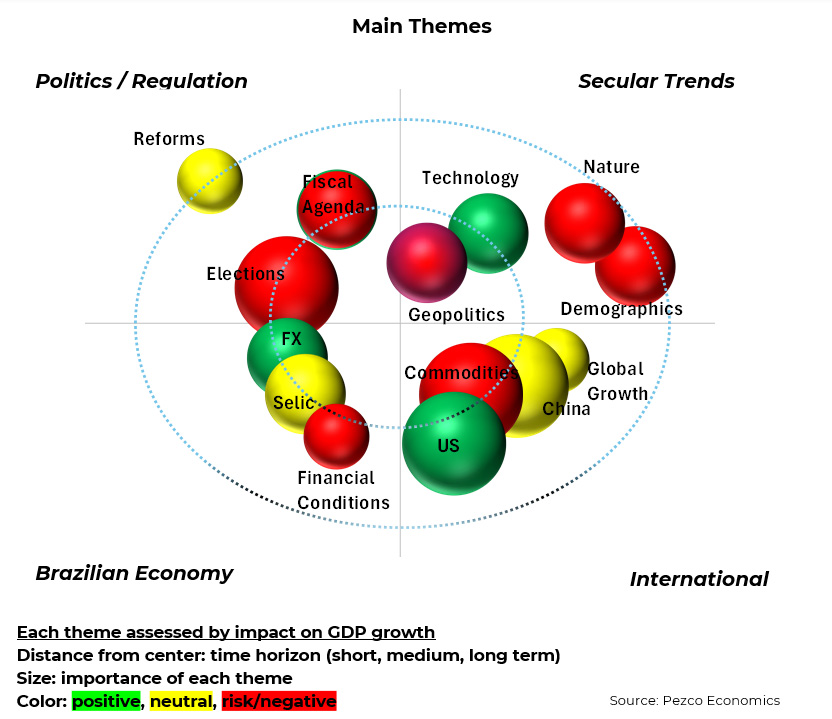

Secular Trends (pg2): Demographics, Geopolitics, Technology and Nature.

International (pg3):. Global Growth, China, The US and Commodities.

Politics / Regulation (pg4):.2026 Elections, Fiscal Agenda and Reforms.

Local Economy (pg.5): FX, Interest Rates / Inflation and Financial Conditions.

Secular Trends

Demographics. Aging population in advanced economies and in Brazil itself is likely to reduce potential growth by slowing the expansion of the working-age labor force. Additionally, it exacerbates fiscal imbalances and ideological polarization, increasing the likelihood of financial and political instability. The baseline scenario assumes no major crises in 2026, but the ongoing deterioration raises the risk.

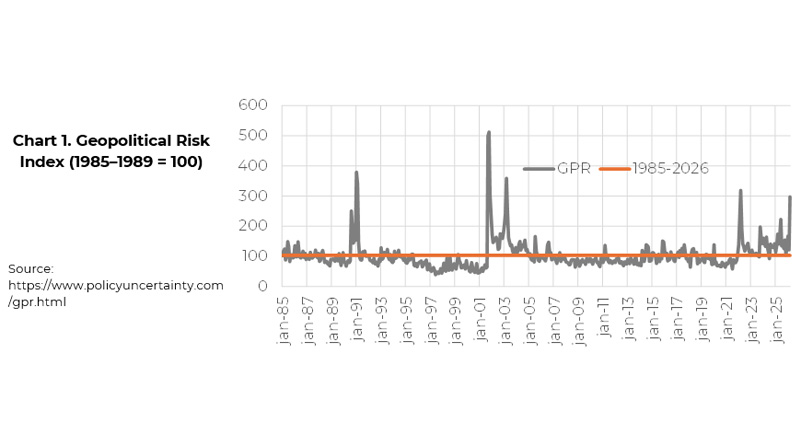

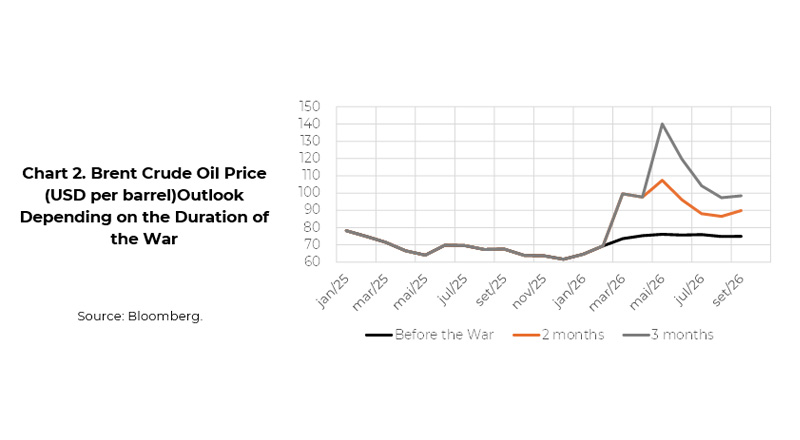

Geopolitics: The dispute for global economic hegemony between the United States and China, as well as the war between Russia and Ukraine, have moved to the background. The U.S. attack on Iran now stands as the main geopolitical risk factor. The scenario assumes more intense conflicts for about two months, easing from April/May onward.

Nature: Global warming and climate variability can generate extreme events that affect food supply. The baseline scenario does not incorporate such a shock in 2026. For 2027, the outlook is likely to be different. The National Weather Service (the official provider of climate forecasts for the U.S. government) expects a transition from La Niña to neutral conditions in the coming months, followed by El Niño in the second half of the year (bringing drought to Southeast Asia, Australia, and Brazil’s North/Northeast, and excessive rainfall in the South of Brazil, as well as in Argentina and parts of the United States). If this materializes, food prices are likely to come under upward pressure next year.

Technology: Artificial intelligence is beginning to reshape production and consumption patterns, already generating productivity gains and supporting higher rates of non-inflationary growth, particularly in the United States. The wealth effect generated in equity markets contributes to a favorable outlook for global growth in the coming years (although less so in 2026, due to war).

International

Global Growth: Uncertainty surrounding U.S. economic policy has been offset by the strength of technological innovation. Tariff policy and the depreciation of the dollar have had only a limited upward impact on inflation and interest rates. The conflict in the Gulf, with the resulting increase in oil prices, is likely to constrain monetary policy in several countries and lead to a downward revision of global growth projections from 3.3% to 2.9% in 2026.

China. The trend is toward a continued slowdown, driven by contradictions within the model itself: excess capacity, high indebtedness (particularly in the real estate sector), structural weakness in domestic consumption, population aging, and a weakening of rural-to-urban migration, among others. Added to this are U.S. efforts to limit the expansion of China’s economic, political, and technological influence globally.

Commodities. U.S. attacks on Iran are likely to keep oil prices elevated for some time (see Chart 2). This geopolitical component, together with the likely end of the downward cycle in international agricultural commodity prices, is expected to put upward pressure on inflation. As for iron ore, the start of operations at the Simandou mine—the world’s largest mining project, located in Guinea and led by Chinese state-owned consortia—has the potential to keep prices contained.

The US. The outlook is for somewhat more moderate growth, reflecting the lagged effects of past monetary tightening and the rise in fuel prices caused by the war. Inflationary pressures (wages, tariffs, and dollar depreciation) are likely to prevent further interest rate cuts in 2026. The backdrop remains one of a weakening U.S. dollar, to be reversed only when and if the monetary authority reaffirms its commitment to the 2% annual inflation target.

Politics and Regulation

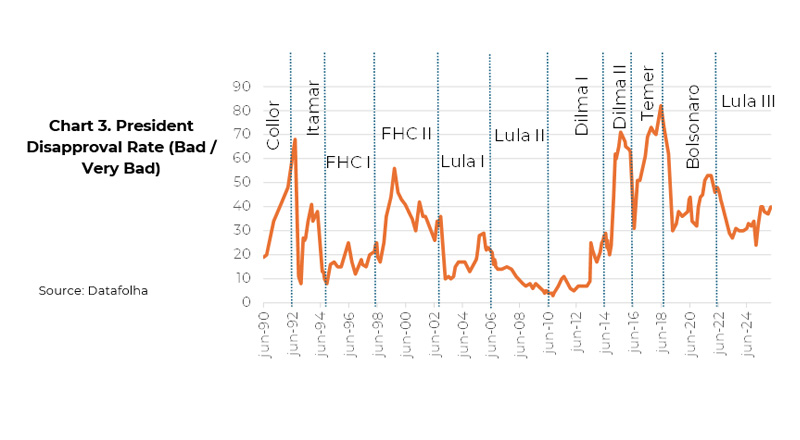

2026 Elections: Financial asset prices are likely to react increasingly strongly to evolving expectations regarding the economic agenda that will prevail in the 2026 election. We have argued that the skepticism and conservatism of Brazilian voters tend to create challenges for the incumbent, who may respond by proposing populist measures (fuel subsidies, a 6×1 workweek structure, debt renegotiation, etc.). The prospect that a more austere fiscal framework will be implemented in 2027 should help keep the Brazilian currency supported throughout 2026.

Fiscal Agenda: The outlook for public debt remains challenging. GDP is expected to continue being supported by fiscal and quasi-fiscal impulses, which in turn sustain higher interest rates and rising indebtedness (for the government, corporations, and households). The budget projects a primary surplus of 0.25% of GDP for the federal government, but the year is likely to end with a deficit of around 0.5% of GDP (excluding adjustments, incorporating more realistic assumptions, and adding the results of states and municipalities). Higher oil prices are expected to generate additional revenues of around BRL 15 billion over the year (BRL 11 billion for every USD 10 increase over 12 months), which are likely to be spent on fuel subsidies for gasoline and diesel.

Structural Reforms: The focus of parliamentary activity will be on the elections. On one hand, the government will seek to approve the end of the 6×1 workweek structure, while the opposition will attempt to push forward an investigation into the Banco Master scandal. The electoral agenda makes it difficult to advance reforms in 2026. The main regulatory theme will likely be the first phase of the implementation of the tax reform, whose effects will still take time to be felt in the economy (only from 2032, after the transition period, will the new system be fully in place). The post-election agenda is expected to include Administrative Reform (mainly addressing fringe benefits), a new round of Pension Reform (tackling the indexation of benefits), and a reform of the fiscal framework.

Local Economy

FX: High interest rates in Brazil, favorable flows to emerging economies, the depreciation of the U.S. dollar in international markets, and even the higher oil prices, all support a stronger Brazilian real. Changes in the global backdrop or in market tolerance regarding fiscal prospects could reverse the recent strengthening trend, but we believe it is more likely that the exchange rate will move toward BRL 5.00 per USD in the coming months.

Inflation and Interest Rates: The oil shock will be inflationary. Considering gasoline, diesel, and pass-through effects along the supply chain, we estimate that a new assumption of Brent prices around USD 85 between May and December (instead of USD 68) could increase the 2026 CPI projection by 1.4 percentage points. The government is working to mitigate this impact through subsidies, tax breaks, and by freezing Petrobras gasoline prices. The revised exchange rate projection, about 7% stronger than previously assumed, also helps contain the impact of rising fuel prices. Overall, inflation is expected to be around 0.5 percentage points higher than previously projected. This, of course, affects the expected path for the Selic rate, which should still decline, but at a slower pace.

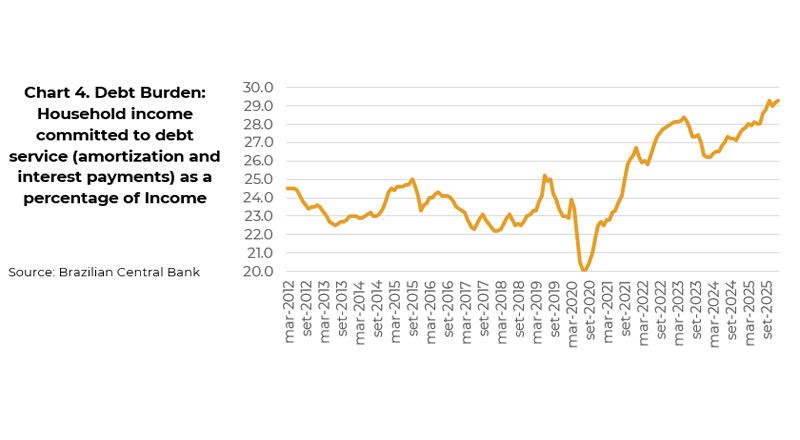

Financial Conditions: Household income committed to debt service (amortization and interest payments) remained stable at 29.3% in the January reading, the latest available (see Chart 4). This level is extremely high: it fluctuated between 22% and 25% for ten years up to 2021, but surged after COVID-19. The financial burden will certainly pose a challenge to the recovery of consumption and may even influence elections.

Forecasts

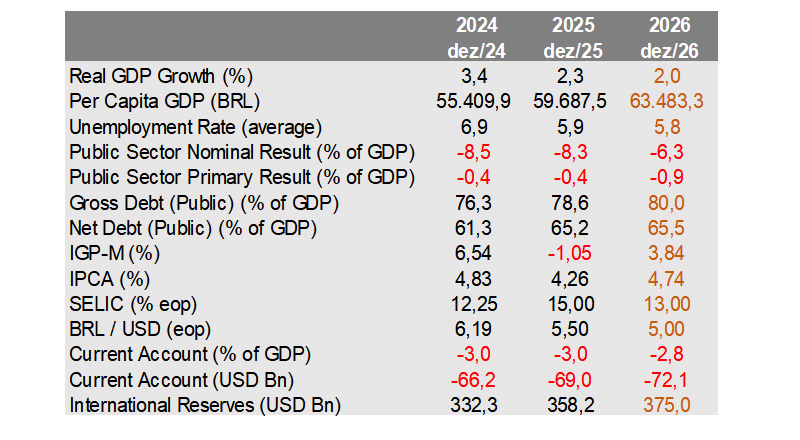

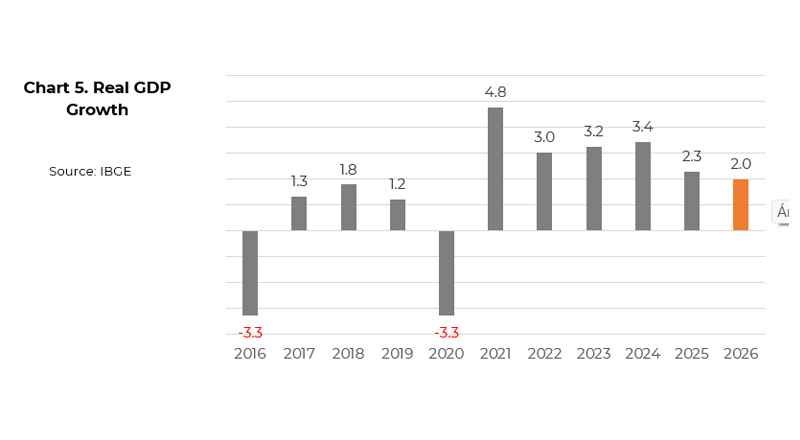

GDP: The dynamics of GDP growth is expected to feature a reasonably strong rebound in the first quarter of 2026, followed by more moderate expansion in subsequent periods. Fiscal and quasi-fiscal impulses, in contrast to tight monetary policy, are likely to support economic activity. The oil shock has led us to revise our 2026 growth forecast down from 2.5% to 2.0%.