- Current account transactions recorded a deficit of USD 5.6 billion in February 2026. Foreign direct investment (FDI) posted net inflows of USD 6.8 billion. Portfolio investment in the domestic market registered net inflows of USD 5.4 billion, of which USD 2.8 billion in equities and investment funds and USD 2.6 billion in debt securities. Over the twelve months ending last month, portfolio investment in the domestic market totaled net inflows of USD 29.3 billion.

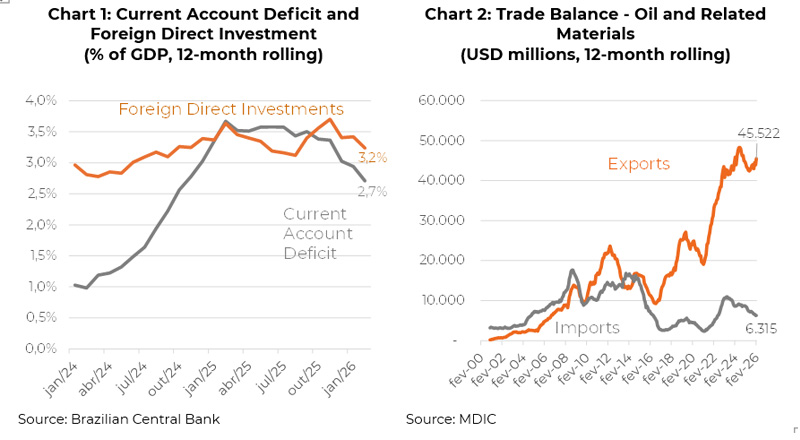

- Although not yet incorporating the period following the oil shock, external accounts data indicate that Brazil is well positioned to weather the international crisis. First, the current account deficit, at 2.7% of GDP on a 12-month basis through February, has narrowed significantly from the 3.6% level prevailing in mid-2025 (Chart 1).

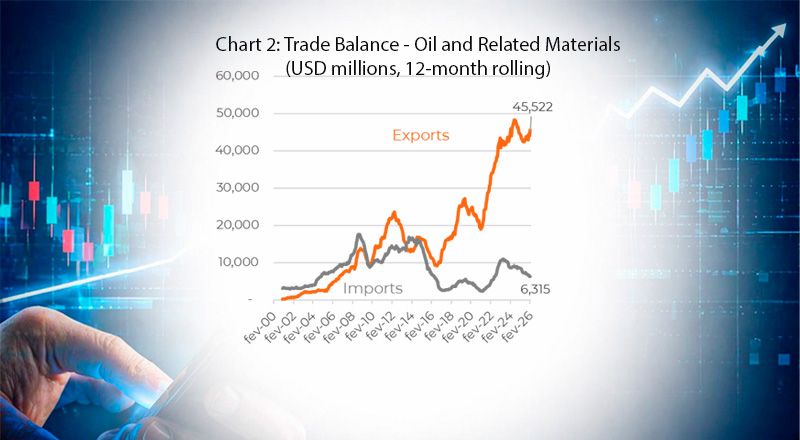

- Second, the positive balance between oil exports and imports continues to expand (Chart 2). If prices average USD 100 per barrel (Brent) through year-end, the trade balance could receive a positive boost of USD 13 billion in 2026 alone.

- Indeed, oil is already among Brazil’s main export products, and the trend points to further growth, at least through 2028. In the context of a price shock stemming from the conflict in Iran, the country’s position as a major producer is also likely to have a positive impact on fiscal accounts. For every USD 10 increase in oil prices, the impact on net public sector revenues could reach BRL 11 billion over a one-year horizon.