Debt and Delinquency Remain at Concerning Levels

- Despite the exchange rate appreciation, which reduced the stock of non-financial sector debt denominated in reais, both indebtedness and delinquency levels remained at concerning levels in January 2026. The situation is likely to worsen (with the economic slowdown) before improving (with lower interest rates).

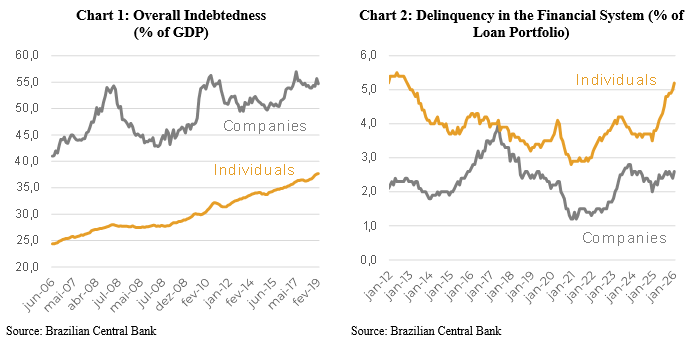

- The outstanding stock of broad credit to the non-financial sector totaled BRL 20.8 trillion (162.6% of GDP), slightly below (-0.3%) the level observed in the previous month.

- Credit supply from the financial system remains predominantly strong in earmarked lending modalities, with year-over-year growth of 12.6% compared to 8.3% for free-market credit. Overall credit increased 10.1%.

- The average delinquency rate in the corporate segment reached 2.6% of total loans, up from 2.0% a year earlier. However, recent dynamics have been characterized by relative stability. For households, however, delinquency remains on a strong upward trend, reaching 5.2% in January, compared to 3.0% in the same month of the previous year (Chart 2).

- Household debt burden (principal and interest payments) remained stable at 29.2% in the latest available reading (December). This level is extremely high: it fluctuated between 22% and 25% for ten years until 2021 but surged after COVID-19.

- The financial burden will likely pose a challenge to the recovery of consumption and may even influence elections.

| This report was prepared and published by the team of partners and consultants of Pezco Consultoria, Editora e Desenvolvimento Ltda (“Pezco Economics”), exclusively for its clients and partners. This document is intended to serve as a basis for discussion of elements of the economic and sectoral environment, through the compilation of information and the presentation of analyses and viewpoints. Every effort has been made to ensure the reliability of the information and its sources; however, the accuracy of such information or of the analyses derived therefrom cannot be guaranteed. All information contained herein that is characterized as a “projection” or “forecast” is based on elements and trends available at the time the analysis was produced, the underlying assumptions of which may change significantly over time. This document is not intended to offer or solicit the purchase or sale of any goods or services. Pezco Economics and the professionals who participated in the preparation of this report accept no responsibility for decisions taken on the basis of this document. Both Pezco Economics and the partners and consultants named in this report may hold positions in assets mentioned herein, and may be participating or may have participated in consulting or advisory projects related to the organizations mentioned. In such cases, the analyses presented disregard any non-public information protected by confidentiality agreements. This report may not be reproduced or redistributed, in whole or in part, for any purpose whatsoever, without the prior written consent of Pezco Economics. |