Inflation Projections Continue to Decline. FX Begin to Adjust

- We have been highlighting three extremely important dynamics regarding financial market projections:

- The consolidation of the exchange rate at around BRL 5.20/USD had been slow to affect the median estimates. Not anymore. The consensus for end-2026 declined from BRL 5.50/USD to BRL 5.45/USD over the past two weeks. It will continue to fall.

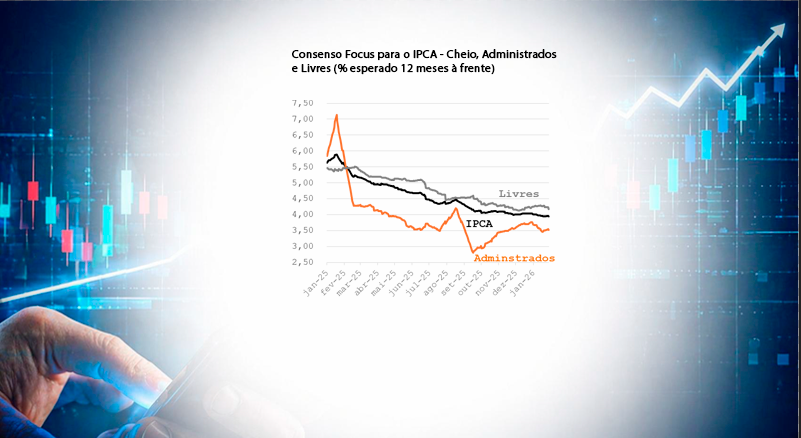

- Inflation projected for the current year has been declining for seven consecutive weeks (3.91% in the latest reading) but has not yet affected expectations for 2027 (stable at 3.80% for 16 weeks). It is only a matter of time

- Lower exchange rates and inflation are already leading to revisions in Selic rate projections: 12.125% for 2026, down from 12.50% in the previous week. It is expected to decline further.

- An important detail is that inflation estimates remain significantly lower for administered prices than for free-market prices (Chart 1). This poses a particular challenge for the convergence of expectations toward the target.

- GDP consensus remains broadly unchanged (1.82% for 2026, 1.80% for 2027, and 2.0% for 2028). Analysts seem to strongly believe this corresponds to the economy’s potential growth rate—quite weak for a country with Brazil’s social demands.

- The current account deficit in 2026 (USD 67.7 billion) remains comfortably financed by the consensus for foreign direct investment (stable at USD 75 billion).

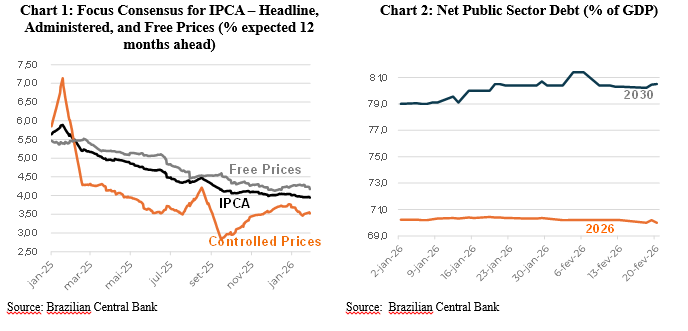

- Expectations regarding fiscal dynamics reflect a well-established pessimism. Even as the market improves projections for various macroeconomic variables in 2026, the consensus points to a further deterioration in the expected long-term public debt trajectory. This is, without a doubt, the main macroeconomic issue to be addressed after the elections (Chart 2).

This report was prepared and published by the team of partners and consultants of Pezco Consultoria, Editora e Desenvolvimento Ltda (“Pezco Economics”), exclusively for its clients and partners. This document is intended to serve as a basis for discussion of elements of the economic and sectoral environment, through the compilation of information and the presentation of analyses and viewpoints. Every effort has been made to ensure the reliability of the information and its sources; however, the accuracy of such information or of the analyses derived therefrom cannot be guaranteed. All information contained herein that is characterized as a “projection” or “forecast” is based on elements and trends available at the time the analysis was produced, the underlying assumptions of which may change significantly over time. This document is not intended to offer or solicit the purchase or sale of any goods or services. Pezco Economics and the professionals who participated in the preparation of this report accept no responsibility for decisions taken on the basis of this document. Both Pezco Economics and the partners and consultants named in this report may hold positions in assets mentioned herein, and may be participating or may have participated in consulting or advisory projects related to the organizations mentioned. In such cases, the analyses presented disregard any non-public information protected by confidentiality agreements. This report may not be reproduced or redistributed, in whole or in part, for any purpose whatsoever, without the prior written consent of Pezco Economics.