- What happens when fiscal stimulus and directed credit expansion are excessive? The answer: the monetary authority is forced to maintain excessively high interest rates to contain inflation, which worsens the financial situation of both households and firms.

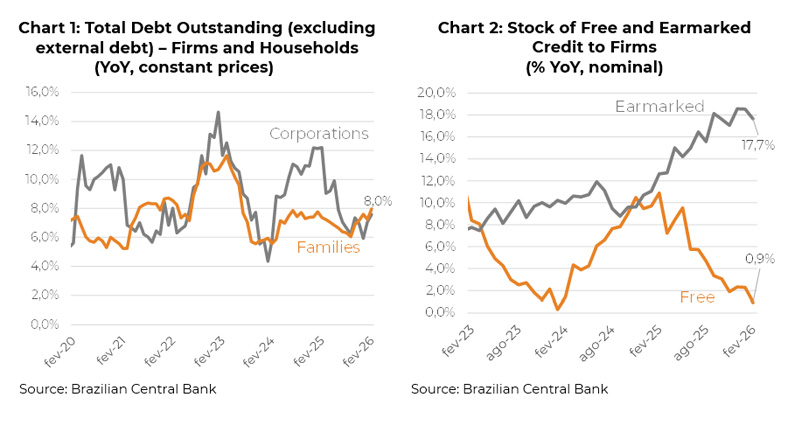

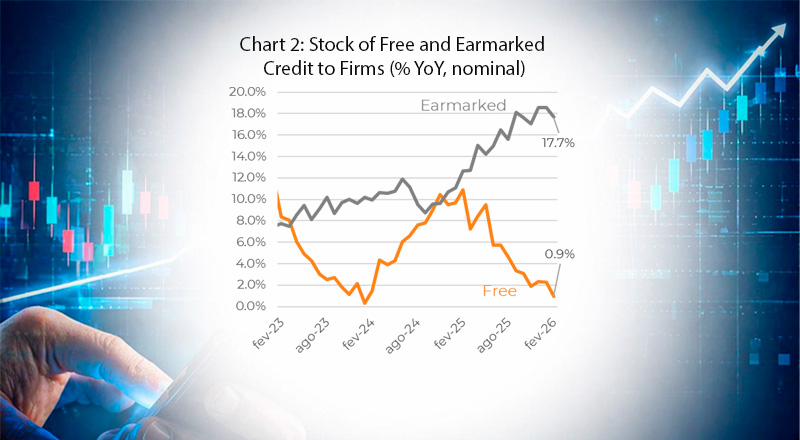

- This is what today’s credit data show. Household and corporate indebtedness is rising at a pace of 7% to 8% per year above inflation (Chart 1). Fiscal stimulus generates excess demand for goods and services, but also for credit. Moreover, the expansion of directed lending more than offsets the transmission of monetary policy through free-market credit within the financial system (Chart 2).

- The problem is that this model is unsustainable. Financial tightening for both households and firms is already becoming a problem. The burden is reflected in both the stock and the cost of debt.

- Total credit operations of the National Financial System reached BRL 7.1 trillion in February, up 9.5% year-over-year, with +7.4% for corporates and +11.2% for households. The non-performing loan (NPL) ratio of the overall credit portfolio rose 0.2 percentage points in the month to 4.3%, with increases of 0.2 p.p. for both corporate and household segments, reaching 2.6% and 5.2%, respectively.

- Household indebtedness stood at 49.7% in January, stable in the month and up 1.1 p.p. over twelve months. The debt service ratio increased 0.1 p.p. in the month and 1.6 p.p. over twelve months, reaching 29.3% of disposable income.