After two months of war and oil prices above USD 100, global inflation has ceased to be merely a risk and has begun to materialize across major economies. Inflation indicators accelerated in the US, Europe, and the UK, increasing pressure on central banks to adopt a more hawkish tone on interest rates.

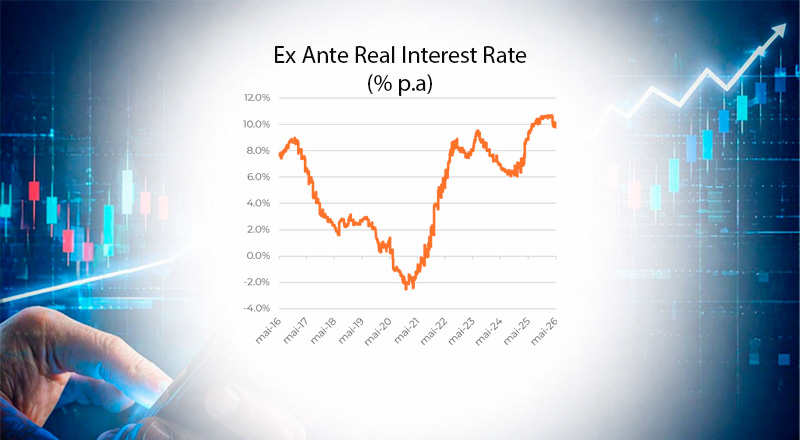

In Brazil, the IPCA-15 inflation index rose to 4.37%, close to the upper limit of the target range, while inflation expectations for 2026 remain above 4.5%. The Central Bank reduced the Selic rate to 14.50%, but maintained a cautious stance amid persistent inflationary pressures. Brazil’s labor market showed signs of cooling, despite unemployment remaining relatively low.

Brent crude oil reached USD 114 per barrel, driven by tensions in the Middle East and uncertainty surrounding the Strait of Hormuz. In financial markets, US stock indices renewed their record highs, while the Ibovespa declined for the third consecutive week.

The Brazilian real appreciated against the US dollar, supported by positive FX flows. We also highlight changes related to Brazil’s tax reform, the impacts of the Mercosur-European Union agreement, and the sharp increase in Chinese exports to South America.

Finally, we emphasize the growing investments by Big Tech companies in artificial intelligence and continue to project moderate growth for the Brazilian economy in 2026.