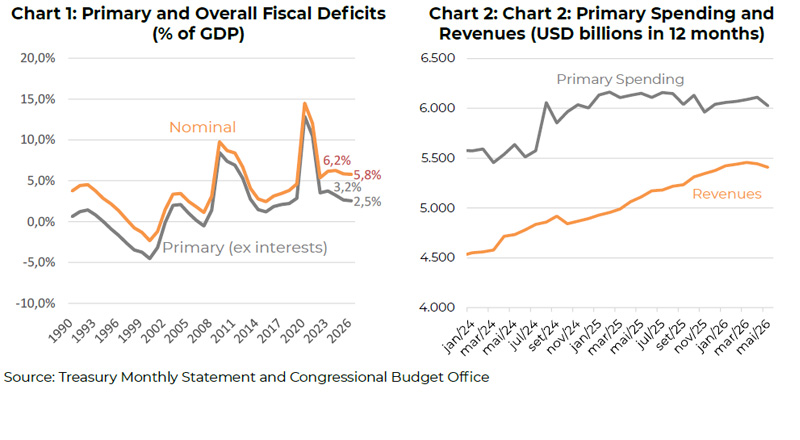

| Although tariffs and a weaker dollar have succeeded in curbing the growth of the trade deficit, it is still unclear whether a lasting improvement in the external accounts has been established for the years ahead. The promise of a more meaningful reduction in public-sector financing needs through spending cuts remained largely unfulfilled. The primary deficit (excluding interest payments) declined from 3.2% of GDP at the end of the Biden administration to 2.7% in 2025 and likely 2.5% in 2026, but this does not appear sufficient to alter the trajectory of the overall fiscal deficit (Chart 1). Moreover, the adjustment has been driven more by higher revenues than by lower spending (Chart 2). The inconsistency of economic policy continues to impose significant costs on American households. Tariffs and currency depreciation have increased the cost of living, while uncertainty and domestic inflation have kept interest rates at their highest levels in more than two decades. |

Introduction

Economic policy initiatives under President Trump’s second term have proven even more unpredictable than during his first administration. The war in the Middle East has undoubtedly been the most important event. The consequences of overall strategy, however, were hardly unexpected from an analytical standpoint.

Uncertainty surrounding geopolitical initiatives has increased asset-price volatility and contributed to the depreciation of the U.S. dollar. This factor may have played a more important role in reducing the trade deficit than the direct effect of higher tariffs. At the same time, neither fiscal nor trade policy appears to have substantially altered the dynamics of the public deficit. Ultimately, the result has been an environment characterized by higher inflation and elevated interest rates.

Foreign Trade: The Trade Deficit Has Stopped Widening

During his second term, President Donald Trump once again placed trade policy at the center of his economic strategy, adopting a strongly protectionist stance. The cornerstone of this approach was the implementation of “reciprocal tariffs,” announced in April 2025, which imposed a minimum tariff rate of 10% on most imports and higher rates on countries deemed responsible for trade barriers or large bilateral surpluses with the United States. The administration justified these measures as a response to persistent trade deficits, the erosion of domestic industrial capacity, and what it viewed as unfair practices by trading partners.

The administration also expanded restrictions on strategic sectors, increasing tariffs on steel, aluminum, and a wide range of manufactured goods, while using trade policy as a tool for bilateral negotiations. The objective was to pressure trading partners into more favorable agreements and encourage the reshoring of industrial production. Some of these measures were later challenged in court, culminating in a Supreme Court ruling that limited the Executive Branch’s ability to impose tariffs under certain legal provisions without explicit Congressional authorization. Nevertheless, most tariffs remained in place, either through legal appeals or through the adoption of alternative legal frameworks. As a result, uncertainty for businesses and investors remained elevated, while trade negotiations with several partners continued.

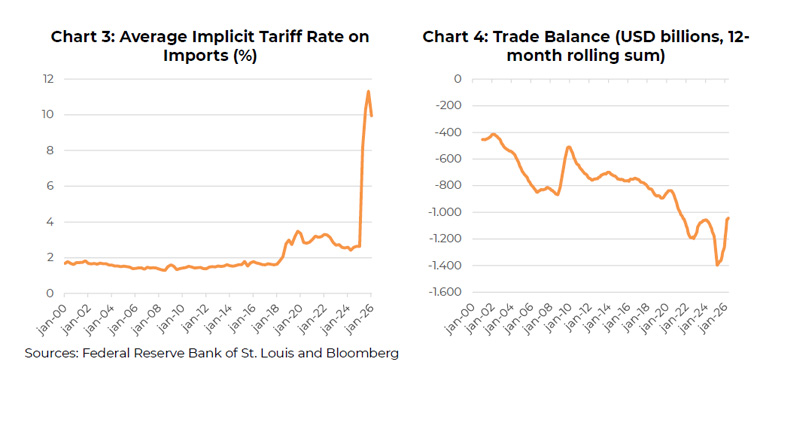

Chart 3 presents an estimate of the average implicit tariff rate applied to imports each quarter, calculated as total customs revenues divided by the value of imported goods. The data clearly illustrates the magnitude of the shock. Chart 4, on the right, shows the 12-month cumulative trade balance.

It is evident that trade policy succeeded in halting the deterioration of the trade deficit. However, it is important to recognize that a significant portion of the worsening observed in late 2024 and early 2025—when the deficit reached USD 1.4 trillion—was driven by front-loaded imports ahead of anticipated tariff increases. Therefore, it is premature to conclude that the trend will continue to improve from here.

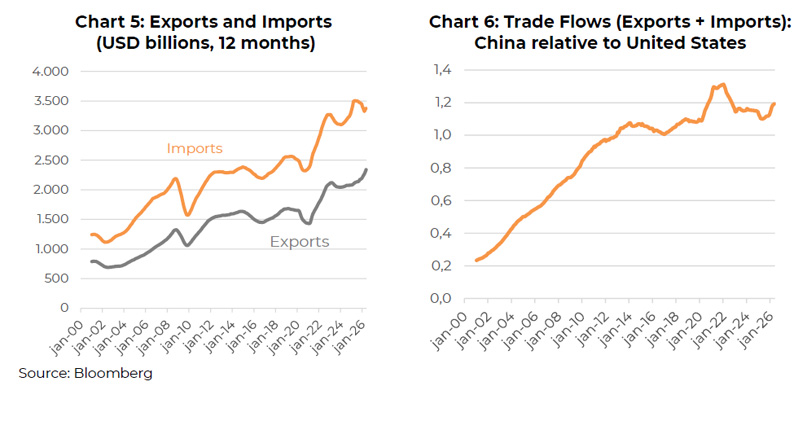

It is also worth noting that the depreciation of the U.S. dollar helped not only to make imports more expensive but also to improve export competitiveness (see Chart 5). Ironically, the decline in the dollar’s value—nearly 10% against the DXY basket during 2025—was itself largely a consequence of uncertainty surrounding U.S. economic policy initiatives, including the erratic implementation of tariffs, which encouraged investors to seek alternative destinations for their capital.

In this sense, the containment of the trade deficit has come at a considerable cost. Higher tariffs and depreciated currency have raised the cost of living. Uncertainty and domestic inflation have sustained higher interest rates. Moreover, there remains a risk that the United States could continue losing ground—and influence—in global trade to China (Chart 6).

A more effective approach to addressing external imbalances would likely have been through fiscal adjustment: reducing the public deficit to allow lower interest rates and a more competitive exchange rate, as lower public dissaving would reduce the need for foreign capital inflows.

A Too Modest Fiscal Adjustment

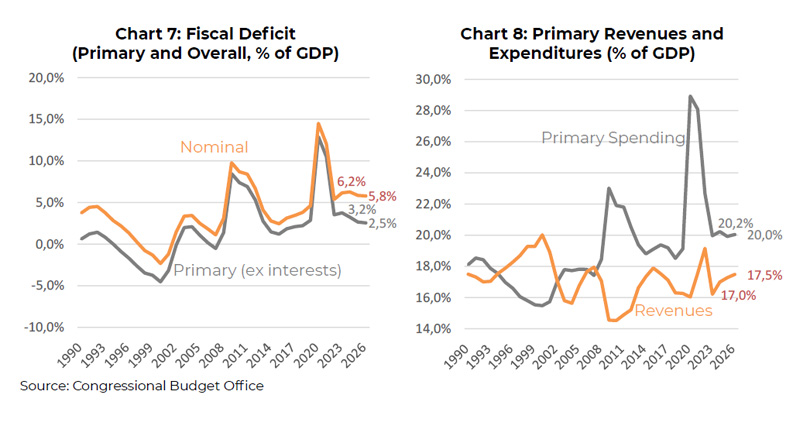

The promise of a more aggressive reduction in public-sector financing needs through spending cuts remained largely unfulfilled. The decline in the primary deficit (excluding interest payments), from 3.2% of GDP at the end of the Biden administration to 2.7% in 2025 and likely 2.5% in 2026, does not appear sufficient to alter the trajectory of the overall fiscal deficit (see Chart 7).

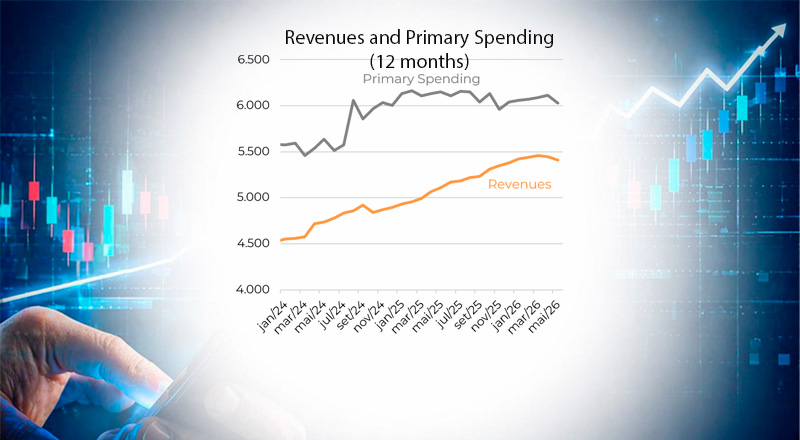

The adjustment has occurred primarily through higher revenues rather than lower spending (Chart 8). Customs revenues, which totaled USD 334 billion in fiscal year 2024 (ending in September), are expected to reach roughly USD 1.4 trillion in 2026. This increase corresponds to approximately 3.3% of GDP and implies there have been tax reductions in non-import-related categories equivalent to roughly 2.7% of GDP, given that the overall tax burden increased by only 0.5 percentage points of GDP.

These figures highlight the central role of trade policy in Trump’s second term. Beyond its effects on competitiveness and domestic production, the tariff strategy has become critical for the fiscal outlook, particularly because policymakers strongly believe that much of the burden is ultimately borne by foreign exporters.

The outlook becomes even less favorable when examining fiscal results at the margin. There appears to be little effort to reduce primary expenditures in nominal terms. The decline in spending as a share of GDP is driven almost entirely by growth in the denominator. Meanwhile, revenue gains are likely to diminish as the marginal contribution of tariff collections becomes increasingly limited.

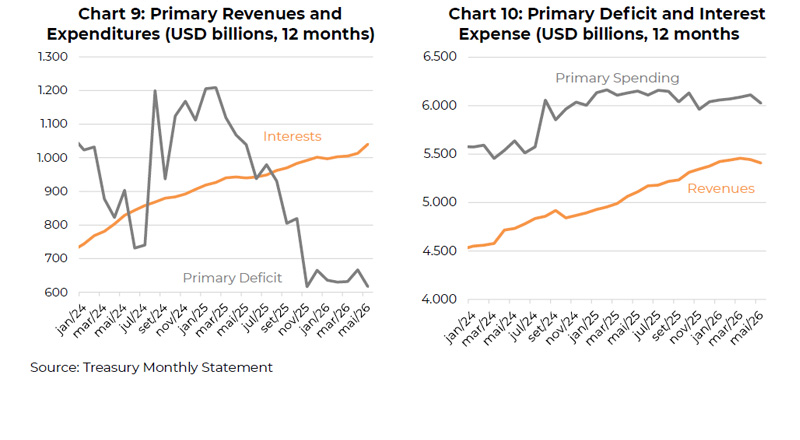

Charts 9 and 10 illustrate this point. The primary deficit appears to be stabilizing at around USD 600 billion per year, while interest expenses continue to rise due to growing indebtedness.

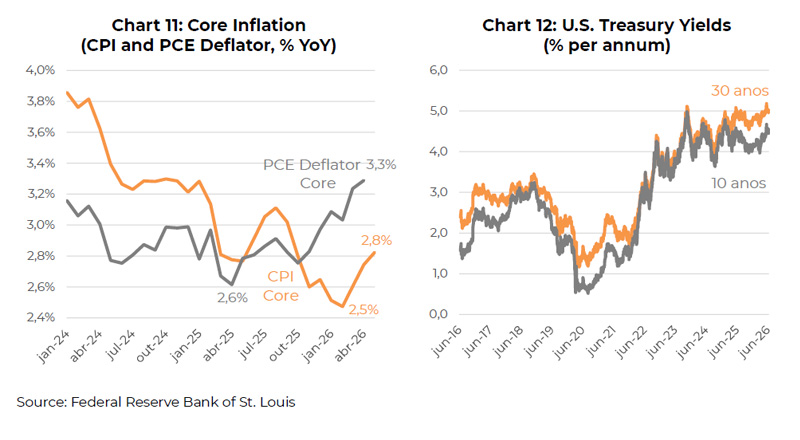

The Result: Higher Inflation and Higher Interest Rates

The strategy of addressing external imbalances through currency depreciation appears counterproductive, insofar as higher inflation requires interest rates to remain elevated for longer.

To be sure, the war with Iran and higher oil prices played a decisive role in pushing inflation upward and leading markets to price in higher policy rates. However, it is equally true that inconsistencies in macroeconomic policy would likely have prevented meaningful Fed easing regardless, as the disinflation process in core inflation had already stalled by late 2025 (see: United States: CPI and PCE Inflation Indicators Pointing in Opposite Directions and Chart 11).lost through the inflationary process, and R$ 220 billion absorbed by investors and bank depositors.

The inflationary impact of tariffs, exchange-rate depreciation stemming from investor uncertainty, and wage pressures in a tight labor market have compounded the fuel-price shock, making it increasingly difficult to envision a scenario in which long-term interest rates decline from their highest levels in more than twenty years (Chart 12).