Monetary and Credit Statistics

- The stock of credit operations within the National Financial System (SFN) reached BRL 7.2 trillion in April, an increase of 9.3% over the past 12 months (against inflation of 4.4%). The main highlight remains the expansion of earmarked credit, which increased 12.2% over the same comparison period. The data make it very clear that the strong impulse to indebtedness is occurring predominantly through public policies, as free-market credit remains far more restrained.

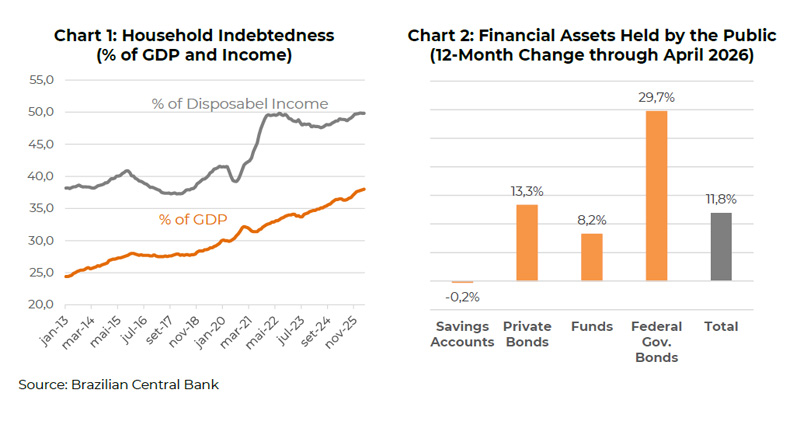

- •Corporate indebtedness remains elevated (54.3% of GDP), although below its historical peak (57%). Household indebtedness, on the other hand, has never been higher (38% of GDP or 49.8% of Disposable Income). Credit costs remain extremely high (an average of 22.3% p.a. for corporations and 39% p.a. for households). Our estimate is that households’ annual interest bill has already reached BRL 1 trillion.

- Delinquency in the household segment continues to break records, and there is no prospect of improvement in the short term: 1) Income gains are likely to decelerate alongside moderating economic growth and an already tight labor market. 2) The pace of cuts in the benchmark interest rate is unlikely to be strong enough to reduce the share of household income committed to debt servicing. And 3) Credit origination continues to grow faster than income, at a pace still consistent with rising indebtedness (see Chart 1).

- We draw attention to the process of significant income transfer from indebted households to saving households (see A Massive Income Transfer). Statistics related to monetary aggregates reinforce this picture: many indebted individuals transferring part of their income to the relatively few holders of financial assets (Non-Financial Private Sector). See Chart 2.