Summary and Conclusions

| The much slower pace of labor supply expansion limits the rate of economic growth consistent with stable inflation. As a result, there are still doubts as to whether the ongoing deceleration in economic activity will be sufficient to bring price dynamics in line with inflation targets, especially in an environment of shock in oil prices. First, because there are still no clear signs of a slowdown in real wage growth. Second, because demographic changes suggest that the magnitude of GDP weakening required to adjust the unemployment rate is now significantly greater than in the past. |

Introduction

In our previous report (The Labor Supply Crisis is Structural), we discussed several dynamics related to Brazil’s labor market, highlighting demographics as the key driver behind the decline in the availability of individuals able to seek employment. We now turn to some of the implications of this structural shift in labor supply, particularly its expected effects on GDP growth and inflation.

GDP and Productivity

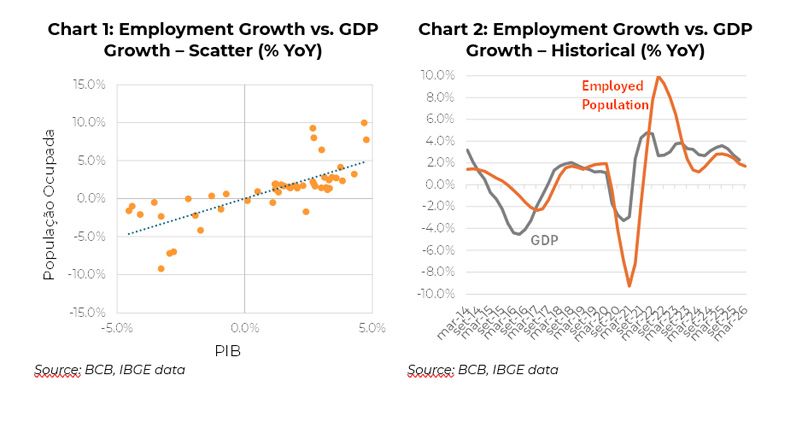

It seems clear that slower labor force growth implies more modest output expansion, unless there are significant changes in capital dynamics (driven by investment) and productivity.

Assuming a labor-output elasticity of around 0.6 within a Cobb-Douglas production function framework, we estimate that the decline in the annual growth rate of the working-age population (WAP), from about 2% at the beginning of the decade to roughly 0.8% currently, could reduce potential GDP growth by approximately 0.6 percentage points over the same period.

Inflation

Constraints on potential growth typically manifest first through inflation. If GDP grows above its potential rate, labor demand tends to exceed supply, pushing unemployment lower. While this is desirable in an environment of high slack (high unemployment), in a tight labor market it tends to generate wage increases above productivity gains, which are usually passed through to prices.

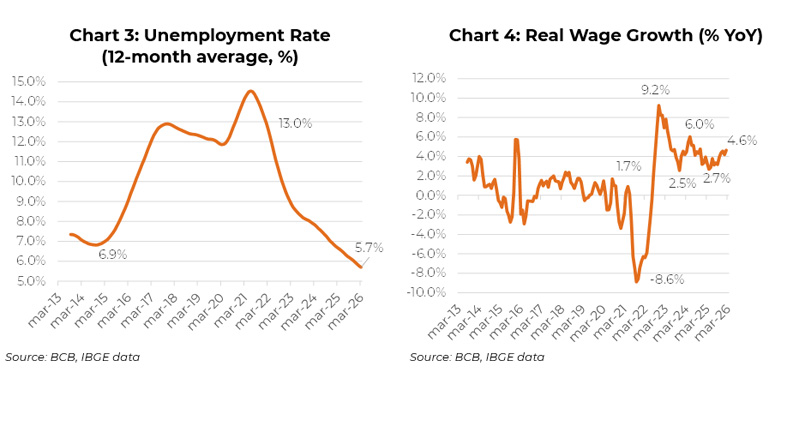

The monetary tightening cycle—more intense in 2022—led to slower growth and a moderation in the pace of decline in unemployment. Real wage growth, which had reached 9% per year as it recovered COVID-related losses, fell to levels more consistent with a disinflationary environment.

However, the strong fiscal and credit impulses observed in recent years continue to boost labor demand in an already tight labor market. Wage pressures remain inconsistent with a sustained decline in services inflation. Currently, the unemployment rate is at its lowest level in the past 15 years (Chart 3), while real earnings are rising at around 4.6% per year (Chart 4).

Monetary Policy

A much slower expansion in labor supply limits the growth rate compatible with stable inflation. Recent data point to a moderation in economic activity in Brazil, but structural constraints in the labor market suggest that this may not be sufficient to bring services inflation in line with targets, particularly in a context of shock in oil prices.

First, as noted, there are still no clear signs of a slowdown in real wage growth. Second, demographic changes imply that a much larger GDP slowdown is now required to adjust the unemployment rate compared to the past.

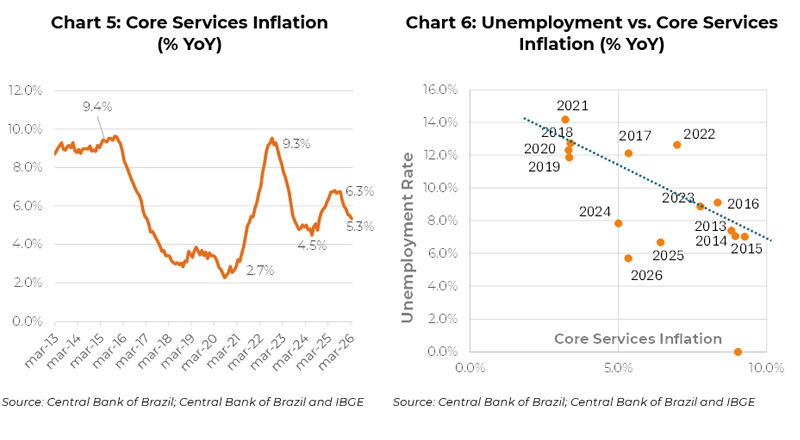

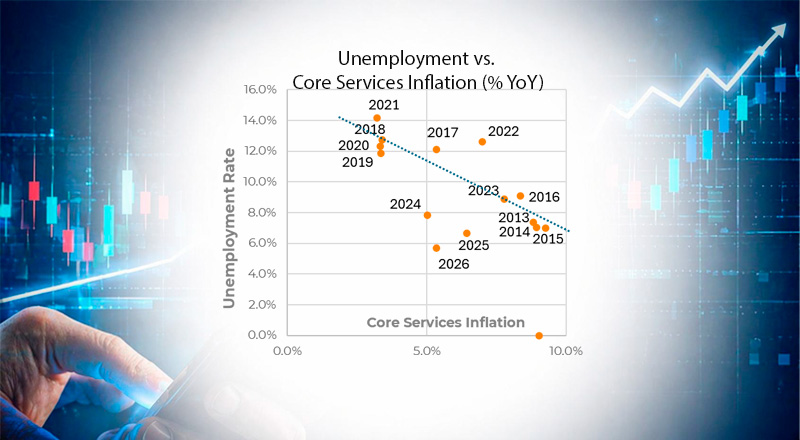

The good news is that, despite these challenges, core services inflation has shown some marginal improvement (Chart 5, next page). There are also signs of improving labor productivity, driven by higher workforce qualification and demographic factors (an older average workforce).

This may help explain why the relationship between unemployment and services inflation has been more benign since 2024 than the average observed over the past 15 years (see Chart 6).