| Demographics, characterized by population aging, have substantially reduced the availability of people fit to work. If we consider a working-age population composed only of individuals between 14 and 64 years old, we observe that the annual growth rate of labor supply has fallen from 1.5 million people at the beginning of the previous decade to around 350 thousand in recent years. This scenario is positive for individuals but challenging for companies and for the monetary authority. Given the prevalence of structural factors, it may now be much more difficult to reduce labor market overheating than it was ten years ago. |

Introduction

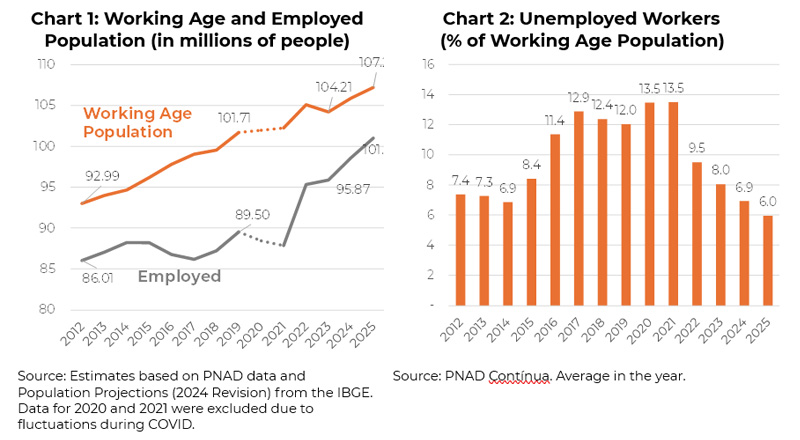

The labor market is tight. There is ample anecdotal evidence of sectors facing difficulties in finding workers. A study by the Central Bank of Brazil indicates that turnover is high and the average wage premium for job switching has fluctuated between 4% and 5% in the formal labor market (based on CAGED data).

The good news is the positive impact on workers’ quality of life, through more jobs and higher wages. The concern lies in the sustainability of this situation. Excessive and persistent inflationary pressures, stemming from an overheated labor market, threaten the growth cycle.

In this piece, we analyze labor supply conditions from the perspective of demographics and the propensity to seek employment.

Demographics

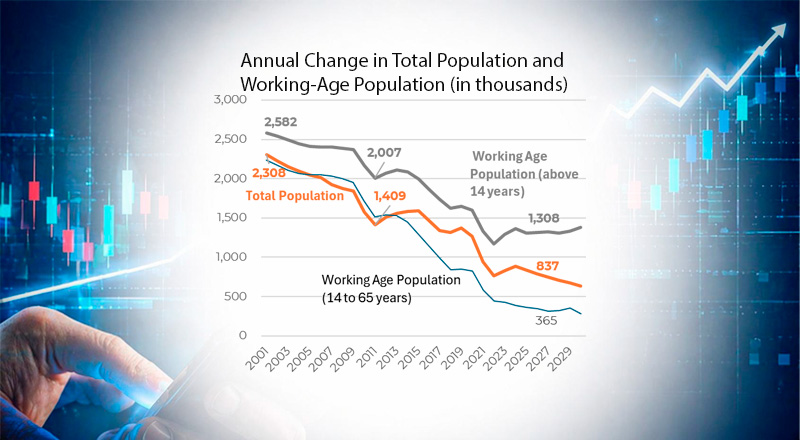

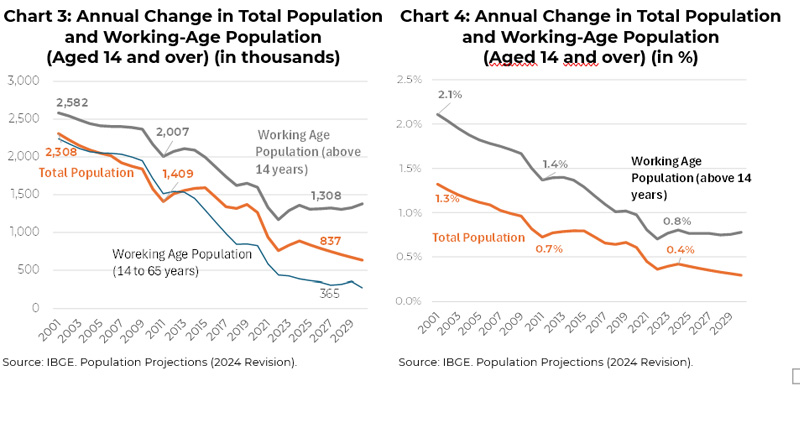

The main driver behind the decline in labor supply is demographic dynamics, long characterized by lower birth rates and higher life expectancy, naturally resulting in population aging. Data show an increasingly slower pace of growth in the potential labor force. Brazil’s total population growth, around 0.7% per year at the beginning of the previous decade, is not expected to exceed 0.4% in 2025. Meanwhile, the working-age population (people aged 14 and over, according to PNAD) is expected to slow more sharply, from 1.4% to about 0.8% per year over the same period.

This implies an additional labor supply of 1.3 million workers per year currently, compared to 2 million in 2010—based on an estimated total population of 214 million and 171 million individuals of working age in 2025.

It is important to note that the growth rate of the working-age population is heavily influenced by the increase in the elderly population. One can perform an exercise assuming a working-age population composed only of individuals aged 14 to 65. This is the concept typically used by researchers to estimate dependency ratios—comparisons between those able to work and those who predominantly study or are retired. In this case, the growth rate of labor supply would drop from 1.3 million to a mere 365 thousand per year.

The previous chart also allows us to assess the impact of COVID on the stock of potential workers. According to IBGE, the growth of the working-age population declined from 1.6 million people per year in 2018–2019 to around 1.2 million in 2022 and 2026.

Demand for Jobs

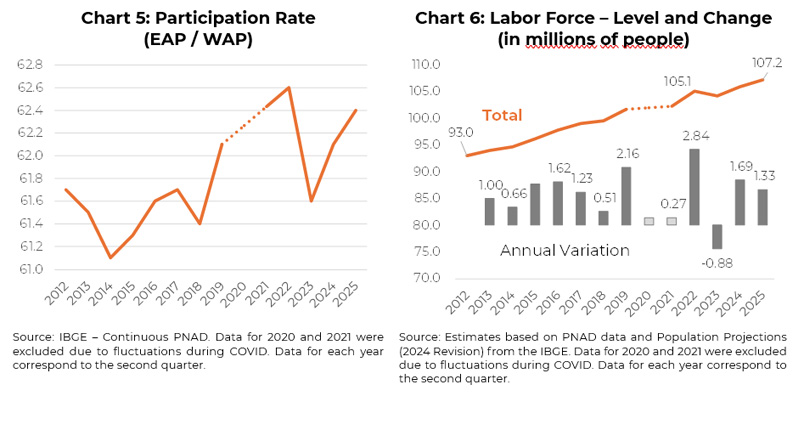

Beyond demographics, there are other factors affecting individuals’ decisions to enter or leave the labor market. A person may choose not to seek employment to invest in education, for example. Alternatively, they may leave domestic activities to pursue a job when opportunities and wages are attractive. Thus, in addition to the pool of potential workers (working-age population), there is the group of people who actually want to work (employed or actively seeking jobs), as opposed to those who prefer other activities (outside the labor force, even if capable of working).

The former group constitutes what is known as the economically active population (EAP). The participation rate is defined as the share of individuals engaged in the labor market (EAP) relative to the pool of potential workers.

Data show a significant decline in the participation rate between 2022 and 2023, possibly linked to the expansion of income transfer programs. It is likely that some individuals have chosen to leave the labor market to receive government assistance, thereby reducing labor supply. The data indicate that nearly 900 thousand people exited the economically active population in 2023.

In 2020, the Emergency Aid program of R$600 per month was introduced, later replaced by Auxílio Brasil. This program initially paid R$400 but returned to R$600 during the elections. In 2023, the Lula administration reinstated the Bolsa Família program and increased the average benefit to R$670 per month. As a result, the number of beneficiaries rose from 14 million in 2019 to 21 million in 2023, with the annual budget increasing from R$35 billion to R$170 billion.

Although social programs may have reduced labor supply, recent years have also shown a significant recovery in the participation rate. This dynamic appears to have been sufficient to bring EAP growth back in line with its previous trend. Indeed, a tight labor market has driven wage increases, attracting individuals who were previously unwilling to compete for available jobs.

Conclusion

The Brazilian labor market has shown signs of tightness, generating inflationary pressures and concerns among companies regarding their ability to attract workers. We highlight the demographic factor—population aging—which has significantly reduced the availability of labor. If we consider a working-age population composed only of individuals aged 14 to 64, we observe that growth has declined from approximately 1.5 million people per year to just 350 thousand.

There is strong evidence that income transfer programs contributed to a further reduction in labor supply. However, more recent data suggest that higher wages may have been sufficient to restore the growth of the economically active population to its recent historical trend.

All of this points to a challenging outlook for labor supply over the coming decades. Structural limitations, linked to demographics, appear more relevant than cyclical factors such as Bolsa Família, COVID, or short-term economic conditions.

This scenario is positive for workers but raises concerns regarding inflation. Given the predominance of structural factors, reducing labor market overheating may now be significantly more difficult than it was at the beginning of the previous decade.