- The producer price index (PPI) came in above expectations in January, adding to the latest personal consumption expenditures (PCE) deflator reading to form a much less benign picture for inflation in the United States. Recent attacks on Iran suggest that the disinflation driven by falling oil prices is likely to be interrupted, at least for a few months, which will certainly affect inflation forecasts and FOMC monetary policy decisions.

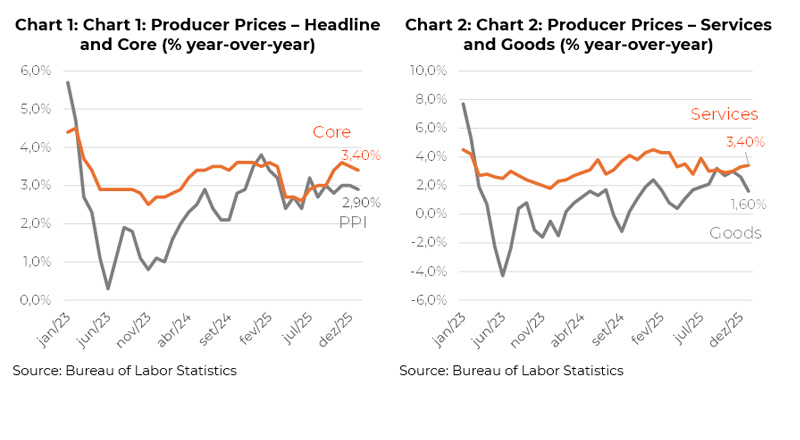

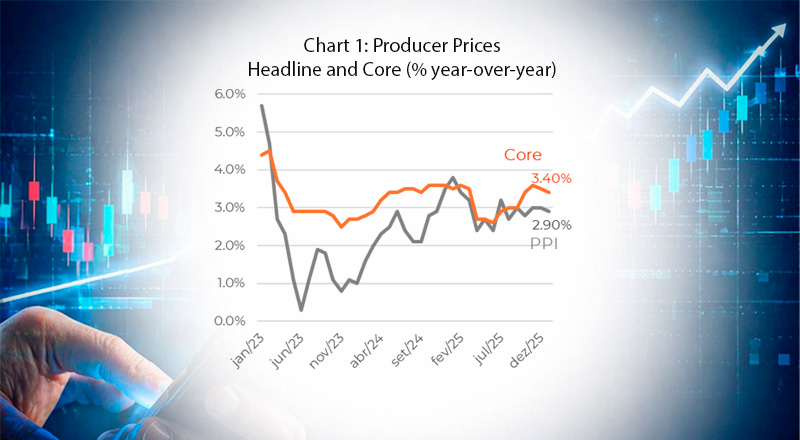

- The U.S. producer price index rose 0.5% in January 2026, following increases of 0.4% in December and 0.2% in November of last year. The year-over-year change was 2.9% for the headline index and 3.4% for the core index (excluding food and energy).

- The producer price index, like its consumer counterpart, is also divided into services and goods. The former continues to drive increases in the index (+0.8% month-over-month), while the latter recorded deflation (-0.3%) in the latest reading. This composition shows that most pressures continue to come from wages, offsetting the disinflationary contribution from imports from China, even amid tariffs and the depreciation of the dollar in international markets. This dynamic is likely to persist.

- It is important to highlight that the decline in gasoline prices observed since 2024 had also been playing a significant role in keeping the goods component in deflationary territory. On a 12-month basis, the energy group fell by 4.4%.

- The reversal in the downward trend of oil prices—already visible in January and intensified by the attacks on Iran—is likely to reverse this situation and put upward pressure on both producer and consumer price indices in the coming months.