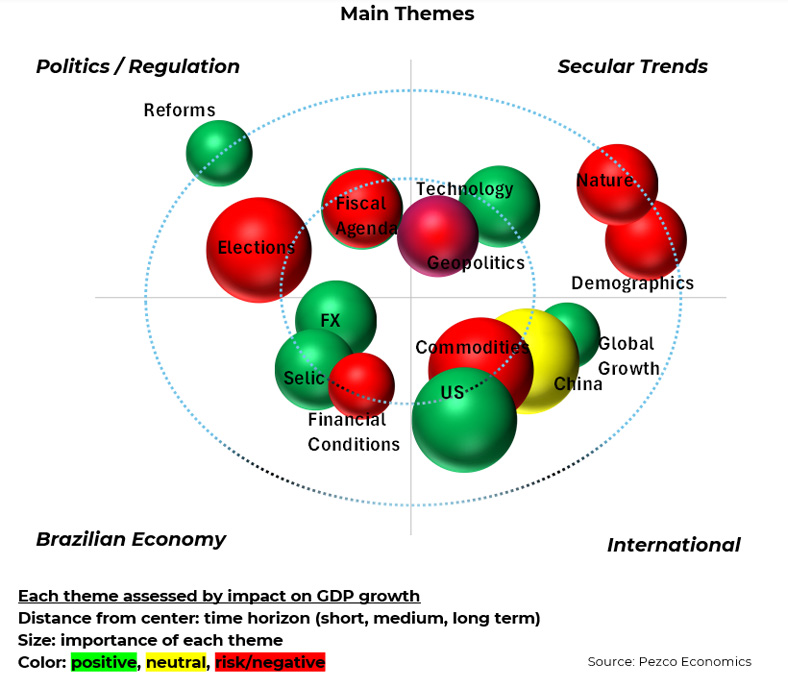

Secular Trends (pg2): Demographics, Geopolitics, Technology and Nature.

International (pg3):. Global Growth, China, The US and Commodities.

Politics / Reguation (pg4):. 2026 Elections, Fiscal Agenda and Reforms

Local Economy (pg.5): FX, Interest Rates / Inflation and Financial Conditions.

Secular Trends

Demographics. Population aging in advanced economies — and in Brazil itself — tends to reduce potential growth by slowing the expansion of the working-age population. Additionally, it exacerbates fiscal imbalances and ideological polarization, increasing the risk of financial and political instability. The baseline scenario assumes no major disruptions, partly because the world is still experiencing a reasonably synchronized monetary easing cycle. Nevertheless, this remains an important risk factor to monitor.

Nature: Global warming and climate variability may generate extreme events and supply shocks, with potential impacts on production and prices, especially commodities. The scenario does not incorporate a major disruptive event, but this remains a relevant risk factor.

Technology: Artificial intelligence is reshaping production and consumption patterns, already generating productivity gains and supporting high non-inflationary growth rates, especially in the United States. The wealth effect generated in equity markets contributes to a favorable outlook for global growth in 2026.

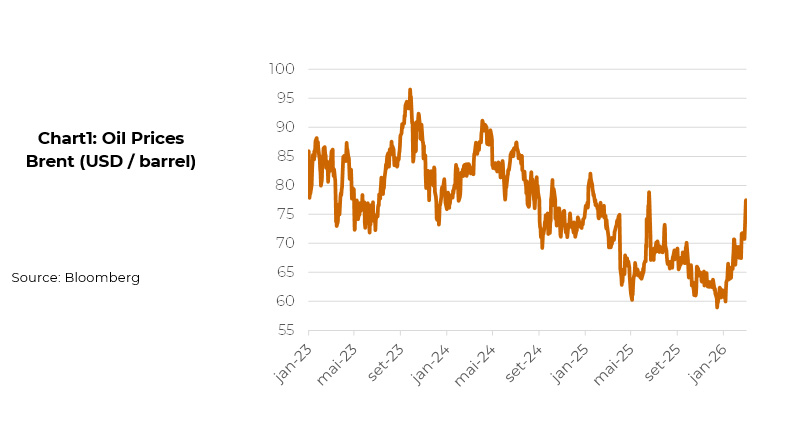

Geopolitics: The dispute for global economic hegemony between the United States and China, as well as the war between Russia and Ukraine, have taken a back seat. The U.S. attack on Iran now emerges as the main geopolitical risk factor. It is possible that, after a few weeks of conflict and higher oil prices, the situation will normalize. However, the risk has clearly increased, and the outlook must now incorporate a shock—albeit temporary—to global fuel prices.

International

Global Growth: Uncertainty surrounding U.S. economic policy has been offset by strong technological innovation, improving the outlook for global economic growth relative to last year. U.S. tariff policy and the depreciation of the dollar in international markets have been less inflationary than expected for global prices or interest rates, supporting a constructive scenario view. The conflict US x Iran, with its repercurssions to oil prices, should be considered an additional source of risk.

Global Growth: Uncertainty surrounding U.S. economic policy has been offset by strong technological innovation, improving the outlook for global economic growth relative to last year. U.S. tariff policy and the depreciation of the dollar in international markets have been less inflationary than expected for global prices or interest rates, supporting a constructive scenario view. The conflict US x Iran, with its repercurssions to oil prices, should be considered an additional source of risk.

Commodities. U.S. attacks on Iran are likely to sustain higher oil prices for some time. This geopolitical factor, together with the likely end of the downcycle in international agricultural commodity prices, substantially reduces the chances of interest rate cuts in the United States. Regarding iron ore, the start of operations at the Simandou mine—the largest mining project in the world, located in Guinea and led by Chinese state-backed consortia—has the potential to keep prices contained.

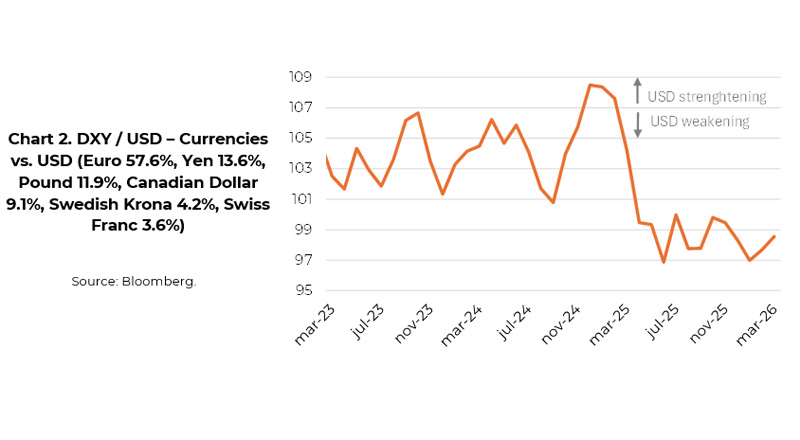

The US. Growth is expected to moderate somewhat due to lagged effects of past monetary tightening and uncertainties related to economic policy decisions (combative rhetoric toward trading partners). Inflationary pressures (tariffs and dollar depreciation) tend to limit room for interest-rate cuts in 2026. The environment still points to a weaker U.S. dollar, which should reverse only when the difficulty of sustaining an optimistic inflation and low-rate scenario becomes clearer.

Politics and Regulation

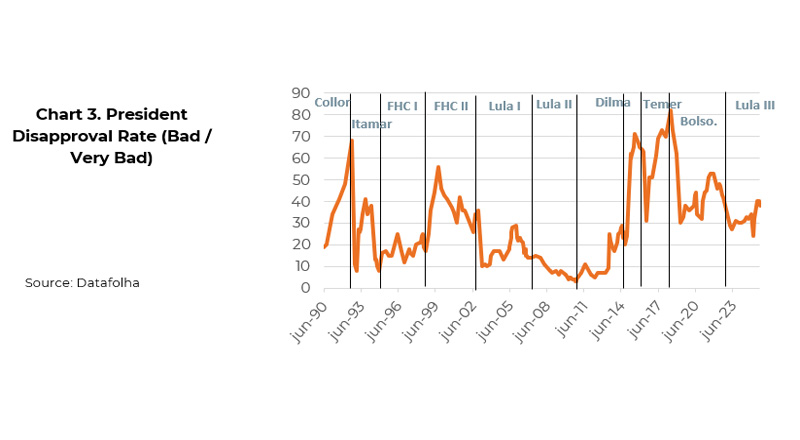

2026 Elections: Financial asset prices are expected to react increasingly to changes in expectations regarding the economic platform likely to win the 2026 election, potentially impacting the currency and short-term growth. The main concern is public debt sustainability. The scenario assumes the issue will be addressed, albeit timidly, insufficient to significantly improve current perceptions.

Legislative Activity: The government will continue attempting to contain fiscal deterioration by increasing revenues. At the turn of the year, important measures were approved, such as: creation of a framework to identify and punish habitual tax defaulters, a 10% cut in tax incentives, higher taxation on betting companies and fintech, The 2026 Budget Law was approved by Congress and sanctioned by the president, setting a surplus target of BRL 34.2 billion, although a more realistic projection points to a BRL 50 billion deficit.

Legislative Agenda: Congressional activity will focus on elections. The government will push to end the 6×1 workweek, while the opposition will seek visibility through the INSS CPI and investigations into the Banco Master scandal. Congress must also ratify the EU–Mercosur agreement. Actions by the Supreme Federal Court should be monitored, especially the advancement of an ethics code, considered the minimum necessary to prevent further deterioration in institutional trust.

Structural Reforms: The proximity of presidential elections makes it difficult to approve reforms in 2026. The main economic topic will be the regulation of the tax reform, whose effects will only be fully felt from 2032 onward, after the transition period. The post-election agenda should include: An Administrative Reform (especially addressing spending cap loopholes), a new round of Pension Reform (indexation of benefits) and a reform of the so-called Fiscal framework, adopted in substitution of the Spending Ceiling framework.

Local Economy

FX: High interest rates in Brazil and dollar depreciation abroad favor real stability at more appreciated levels than last year’s average. This variable is extremely sensitive to financial market sentiment. Changes in the international environment or market tolerance toward fiscal prospects could reverse recent trends. We believe the exchange rate will return to around BRL 5.40 to USD in 2026 due to increasing political uncertainties.

FX: High interest rates in Brazil and dollar depreciation abroad favor real stability at more appreciated levels than last year’s average. This variable is extremely sensitive to financial market sentiment. Changes in the international environment or market tolerance toward fiscal prospects could reverse recent trends. We believe the exchange rate will return to around BRL 5.40 to USD in 2026 due to increasing political uncertainties.

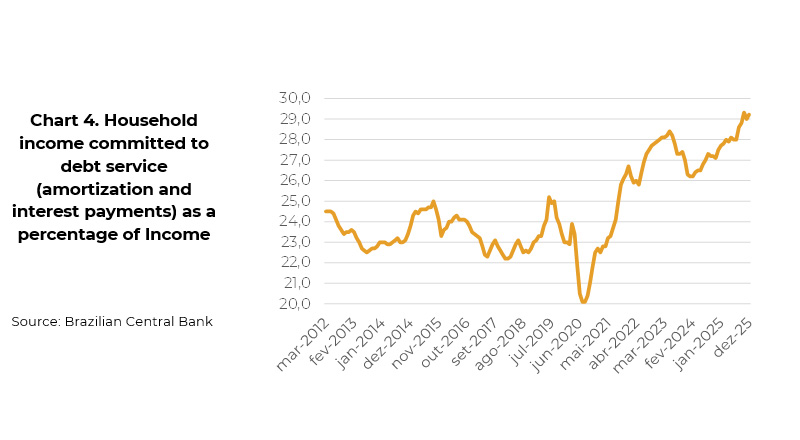

Financial Conditions: Household income committed to debt service (amortization and interest payments) remained stable at 29.2% in the December reading, the latest available (see Chart 4). This level is extremely high: it fluctuated between 22% and 25% for ten years up to 2021, but surged after COVID-19. The financial burden will certainly pose a challenge to the recovery of consumption and may even influence elections.

Forecasts

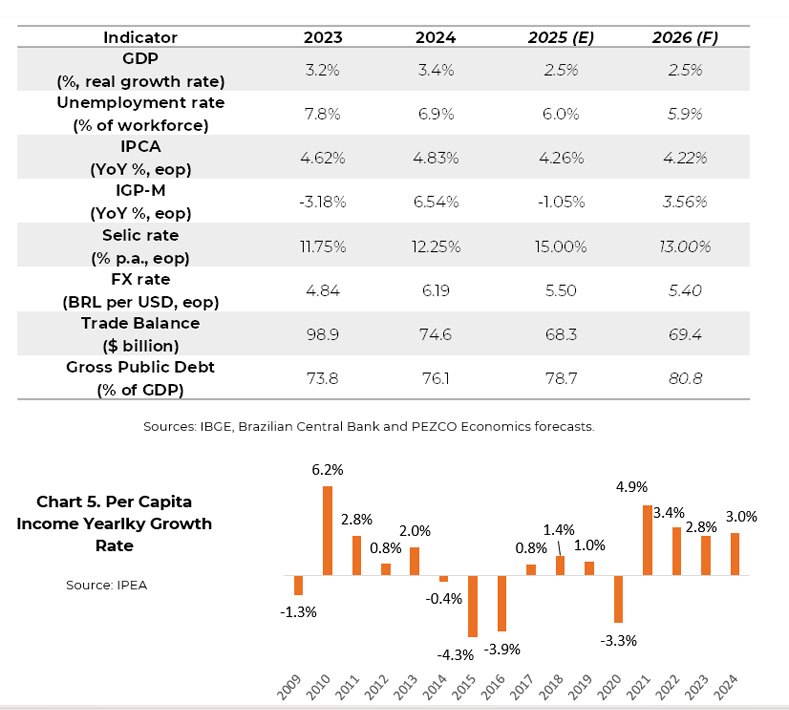

GDP: The GDP dynamics will probably be characterized by a virtual stagnation from 2H25 into 1H26 and and acceleration thereafter. The recovery will depend upon the monetary policy easing cycle to be initiate in 1Q26. We believe infrastructure investents will remain contributing to improve potential GDP growth, which is probably around 3% per year.