Is it possible to identify signs that monetary policymakers are yielding to political pressure and that confidence in maintaining price stability is at risk?

In our view, there are indeed some indications of susceptibility, but with virtually no impact on institutional credibility.

Introduction – The Fed’s Actions and Market Reaction

At the end of January, U.S. President Donald Trump appointed economist and jurist Kevin Warsh as the next Chairman of the Federal Reserve (Fed), the U.S. central bank. He will assume office at a time when the independence of the monetary authority has been called into question due to recurrent attacks from the White House targeting the incumbent, Jerome Powell. But is it possible to identify signs that monetary policymakers are yielding to pressure and that credibility in the fight against inflation is at risk? In our opinion, there are indeed signs of susceptibility, but with almost no impact on institutional credibility.

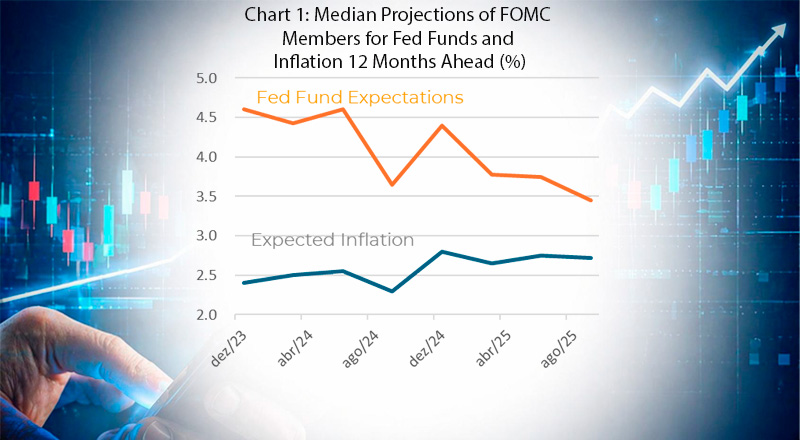

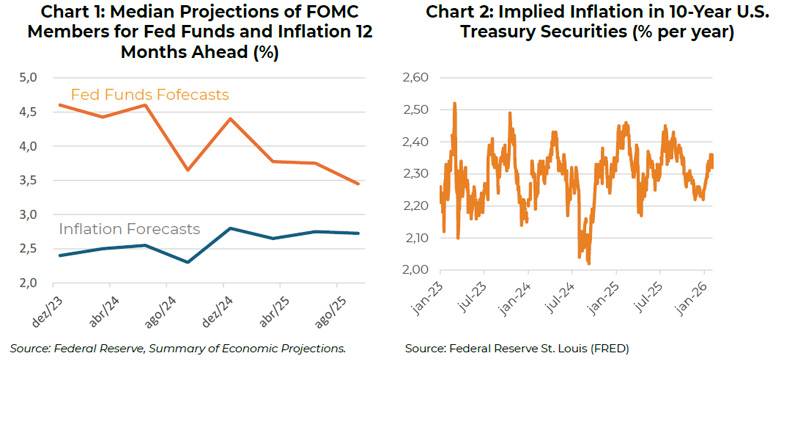

Indeed, the U.S. monetary authority has been questioned to some extent due to the monetary easing cycle engineered during the second half of last year, even though inflation has not only remained stubbornly above target but, at times, moved further away from it, in a context of import tariff shocks. Chart 1 shows the median of the Fed’s own projections for interest rates and inflation 12 months ahead. The figure suggests some increase in tolerance toward the expected acceleration in price growth. In this sense, one cannot rule out the hypothesis that members of the Monetary Policy Committee may have been influenced.

At the same time, however, Chart 2 (to the right) shows that the market has not perceived a loss of credibility on the part of the Fed with respect to its long-term commitment to inflation control. Expectations for the next 10 years, extracted from the yield differential between nominal and inflation-indexed Treasury securities, remain comfortably anchored.

Inflation and Unemployment

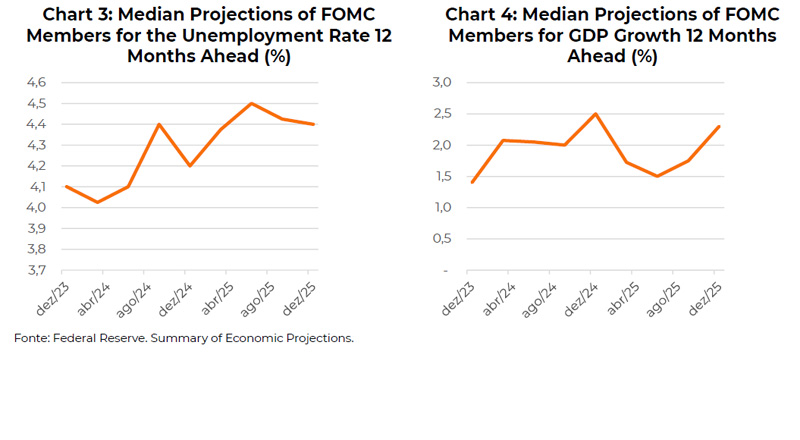

It is undeniable that, despite the deterioration in inflation expectations between 2024 and 2025, partly due to the shock on imports tariffs, the financial market began to forecast increasingly aggressive cuts in the policy rate. This occurred because the monetary authority itself validated this scenario, not only through its actions but also via guidance and projections. It became clear that concern over unemployment dynamics increased, with the median estimate of the Federal Open Market Committee (FOMC) members rising from 4% to 4.5% (Chart 3).

Yet even if there has been a change in the Fed’s reaction function following criticism and threats from the executive branch, no significant deterioration in long-term inflation expectations has been observed, as already noted. The market perceives short-term price shocks as largely transitory, with limited second-round effects (impact on inertia), especially given that the economic slowdown already underway in the second half of the year would help contain price adjustments.

It is quite possible that the so-called “soft landing” does not materialize as envisioned, which may indeed sound too good to be true. Nevertheless, the fact remains that a lower policy rate than previously expected is already in place, reinforcing the perception that GDP will recover and unemployment will decline again (see the charts below).

How the Monetary Policy Committee Operates

One of the factors that has most contributed to sustaining institutional credibility amid so much noise is the increased public exposure of Monetary Policy Committee members. Since mid-last year, they have spoken publicly more frequently. Greater visibility tends to translate into a higher degree of independence: each member becoming more committed to their own past views and publicly stated ideas than to the leadership of the Chairman. This naturally makes dissent more likely.

In total, the voting committee consists of 12 members with equal voting power. In the event of a tie, the decision is to maintain the current policy stance. Although a tie has never occurred, it is generally avoided because the Chairman votes last. It is believed that, on some occasions, final decisions were taken precisely to avoid a deadlock.

Among the 12 voting members, seven are so-called “Governors,” who serve staggered 14-year terms. They are appointed by the President and confirmed by the Senate. The Chairman must be one of these Governors. The fact is that the only term nearing expiration is that of economist Stephen Miran, the most Trump-aligned member and a stronger advocate of aggressive rate cuts. It is his seat that the Senate will consider for Kevin Warsh’s appointment.

Aiming at creating additional vacancies for appointment, President Trump has attempted to pressure two Governors to resign: Lisa Cook and Jerome Powell himself (although Powell’s term as Chairman ends in May, he would still retain voting rights in his capacity as a Governor).

The remaining five voting seats are held by presidents of regional Federal Reserve Banks. There are 12 regional banks, and each president serves a one-year rotating voting term, apart from the President of the New York Fed, who always has voting rights.

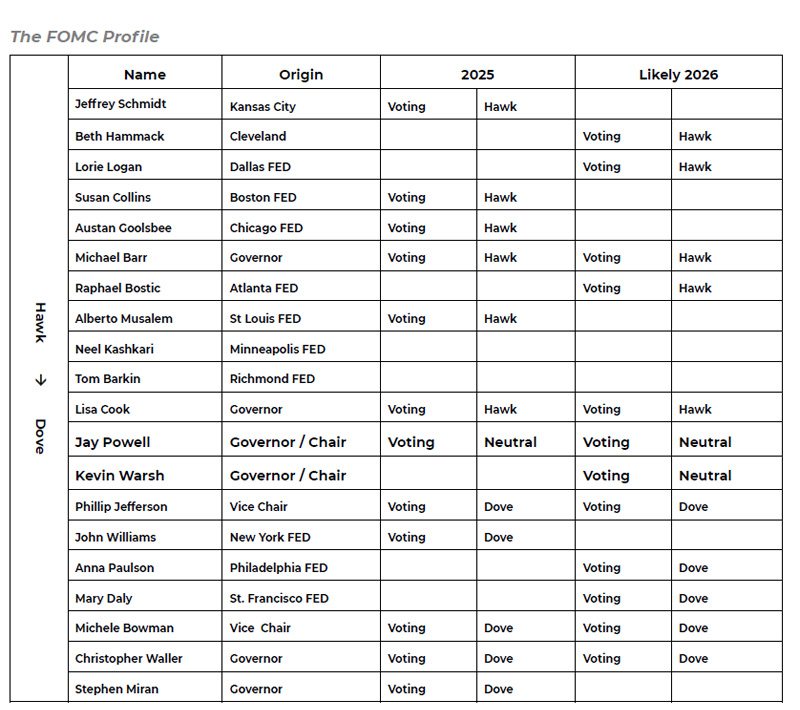

In early December, the British newspaper Financial Times produced a ranking of Federal Reserve Monetary Policy Committee members, ranging from the most conservative (inflation-focused “hawks”) to the most flexible (more tolerant “doves”), based on historical decisions and recent statements.

We reproduce this table at the end of the text (page 4). Acknowledging it clearly involves judgment and abstraction, we also added the board changes expected to occur throughout 2026 and concluded that no significant shift in the committee’s overall profile is likely.

Kevin Warsh

Despite being appointed by Trump at a time of intense pressure to cut interest rates, the market appears to view the new Chairman as a technical figure with strong credentials. One cannot rule out the possibility that, like Powell himself, Warsh ultimately follows a path different from what the White House expects.

Kevin Warsh served as Secretary of the Council of Economic Advisers under President George W. Bush, including during the banking crisis. He resigned in disagreement with so-called quantitative easing, which involved the Fed purchasing assets (Treasuries and mortgages) to inject liquidity into the system. His support for balance sheet normalization is consistent with higher, not lower, long-term interest rates. The newly appointed Chairman advocates tight fiscal policies and opposes deficit monetization.

Regarding the economic outlook, Warsh believes inflation is likely to decline due to productivity gains driven by artificial intelligence. Perhaps for this reason, he may favor more “dovish” decisions in the short term.