As the electoral debate approaches, the discussion surrounding fiscal policy is once again moving to the forefront of market attention. While opinion polls consistently show that healthcare, education, and public safety rank among Brazilians’ top concerns, the fiscal outlook will remain one of the key drivers of financial asset prices, influencing the exchange rate, interest rates, and equity markets.

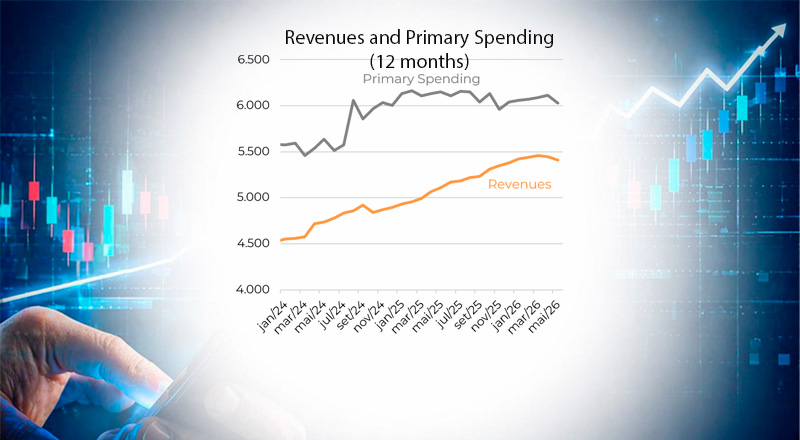

Before discussing solutions, however, it is essential to properly define the problem. This article seeks to contribute to that debate by examining the trajectory of revenues and expenditures of the central government, comprising the National Treasury and the social security system (INSS).

In fiscal discussions, stabilizing the debt-to-GDP ratio typically occupies center stage. If this is identified as the core challenge, it is important to recognize that debt dynamics depend on four key variables: the initial stock of public debt, the primary fiscal balance, the real interest rate, and economic growth. While primary surpluses and economic growth help reduce the debt burden relative to GDP, elevated real interest rates work in the opposite direction. Put simply, the public sector must generate a primary surplus large enough to offset the impact of the interest-growth differential on the existing debt stock. The expansion of quasi-fiscal credit operations ultimately tends to be reflected in the government’s funding costs.

According to my estimates, a primary surplus close to 2.5% of GDP would be required to stabilize public debt at roughly its current level of 80% of GDP, assuming potential growth of 2% per year and convergence of the nominal interest rate to 10%, consistent with a real interest rate of approximately 5%. Given that the public sector posted a primary deficit of 0.97% of GDP in the 12 months through April, the required adjustment would be on the order of 3.5% of GDP, or roughly BRL 455 billion.

Once the magnitude of the challenge is established, it is worth examining some of the most frequently cited proposals in the fiscal debate: limiting minimum wage adjustments to the previous year’s inflation rate; de-indexing healthcare and education expenditures; eliminating the wage bonus program (abono salarial); reducing tax expenditures; and reforming the fiscal framework.

My point is straightforward: all these proposals are relevant, but none is new, and none is sufficient on its own to deliver the adjustment required.

Based on my estimates, changing the minimum wage adjustment rule would generate annual savings of approximately BRL 35 billion. Linking healthcare and education spending solely to inflation would yield savings of roughly BRL 10 billion in the first year. Eliminating the wage bonus program would reduce expenditures by around BRL 20 billion, according to estimates from the Ministry of Finance.

Taken together, these three measures would yield savings of approximately BRL 65 billion, or 0.5% of GDP, in the first year of implementation—well short of the roughly BRL 455 billion adjustment required to stabilize public debt.

Reducing tax expenditures is one of the few measures with the potential to generate an adjustment consistent with the scale of Brazil’s fiscal challenge. In the 2026 federal budget, these tax exemptions are estimated at BRL 612.8 billion, equivalent to 4.7% of GDP. Even excluding programs with strong political support—such as the Simples Nacional tax regime, agriculture and agribusiness incentives, tax-exempt income categories, and the Manaus Free Trade Zone—approximately BRL 300 billion, or 2.3% of GDP, would still remain.

The challenge, however, is political feasibility. Each tax benefit has organized interest groups willing to defend it in Congress and, in many cases, in the courts. Moreover, part of these exemptions was originally created to achieve specific economic objectives, making their elimination even more complex.

Finally, proposals to reform the fiscal framework—such as limiting expenditure growth to the previous year’s inflation rate—could contribute to improving the trajectory of public finances. However, their effects are gradual, depend on the credibility of the government’s fiscal commitment, and require complex legislative approval processes.

The arithmetic is straightforward. The politics are not. The adjustment required to stabilize public debt is substantial. The most frequently discussed proposals in Brazil’s fiscal debate are well known and have been debated by governments across the political spectrum, underscoring the difficulty of translating technical solutions into political reality.