Primary Balance and Debt Dynamics Showing Even Worse Trends

- If it were not for the benign external environment, Brazil would already be facing a confidence crisis regarding its public accounts. The global appreciation of assets in a disinflationary environment, productivity gains driven by advances in artificial intelligence, and portfolio diversification that has contributed to the depreciation of the U.S. dollar in international markets; have generated strong capital inflows, helping to finance the public deficit.

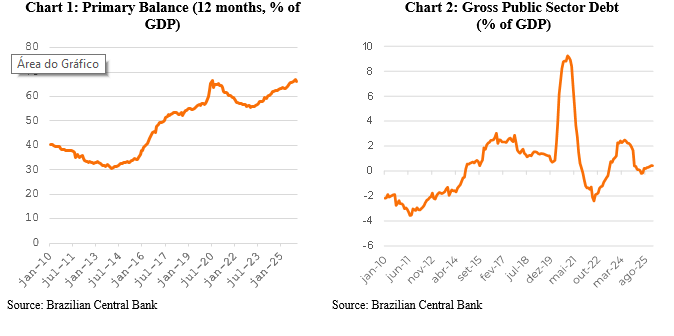

- The consolidated primary deficit over 12 months reached 0.43% of GDP in the twelve months through the end of January, worsening significantly compared to May 2025, when the country posted a primary surplus of 0.2% of GDP (Chart 1).

- The combination of a deteriorating primary balance and high interest rates has also pushed up the nominal result, which reached 8,49% of the GDP in the 12 months ending in January 2026, worse than the 8.34% recorded in the previous month and above the low observed in mid-last year (7.2%).

- Net public sector debt reached 65% of GDP (R$8.3 trillion) in 2025, rising 0,3 percentage points of GDP compared to January 2025. It is important to note that this increase largely reflects the effect of the cumulative exchange rate appreciation of 4,9% Since the Brazilian public sector is a net creditor in foreign currency assets (holding external debt lower than its stock of reserves), any depreciation of the exchange rate helps contain the growth of net debt. Conversely, currency appreciation reduces the value of foreign currency-denominated assets, thereby increasing net debt.

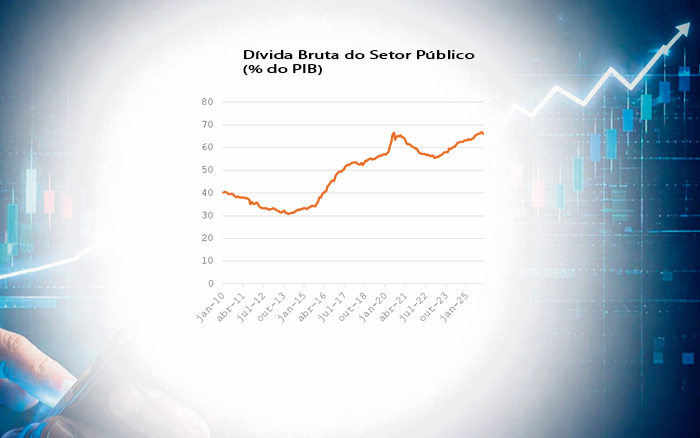

- Gross debt, which is much less directly affected by exchange rate movements, have maintained an upward trajectory (Chart 2), having reached 78,7% of GDP last month, up from 71.5% at the end of 2022. This is a cause for concern.

This report was prepared and published by the team of partners and consultants of Pezco Consultoria, Editora e Desenvolvimento Ltda (“Pezco Economics”), exclusively for its clients and partners. This document is intended to serve as a basis for discussion of elements of the economic and sectoral environment, through the compilation of information and the presentation of analyses and viewpoints. Every effort has been made to ensure the reliability of the information and its sources; however, the accuracy of such information or of the analyses derived therefrom cannot be guaranteed. All information contained herein that is characterized as a “projection” or “forecast” is based on elements and trends available at the time the analysis was produced, the underlying assumptions of which may change significantly over time. This document is not intended to offer or solicit the purchase or sale of any goods or services. Pezco Economics and the professionals who participated in the preparation of this report accept no responsibility for decisions taken on the basis of this document. Both Pezco Economics and the partners and consultants named in this report may hold positions in assets mentioned herein, and may be participating or may have participated in consulting or advisory projects related to the organizations mentioned. In such cases, the analyses presented disregard any non-public information protected by confidentiality agreements. This report may not be reproduced or redistributed, in whole or in part, for any purpose whatsoever, without the prior written consent of Pezco Economics.