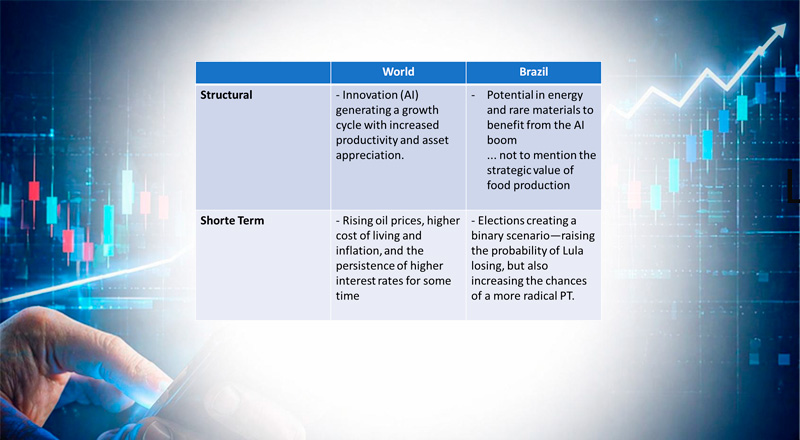

The current macro environment mixes strong structural drivers with adverse short-term shocks.

Globally, AI is fueling a productivity-driven growth cycle, supporting asset valuations.

However, rising oil prices are pushing inflation higher and keeping interest rates elevated.

In the U.S., inflation was already persistent, with additional risks from supply shocks.

As a result, there is little room for rate cuts in 2026.

In Brazil, despite structural strengths in commodities and energy, inflation and high rates remain key constraints.

The political backdrop is increasingly polarized, pessimistic, and prone to radicalization risks.

Economic confidence is also weakened by rising violence, corruption, and institutional concerns.

The growth model appears unsustainable, relying on fiscal expansion and credit amid tight monetary policy.

This has led to higher indebtedness, delinquency, and a more cautious outlook for investments.