It Will Be Difficult for the Fed to Cut Interest Rates in 2026

| Even though markets continue to price in interest rate cuts in 2026, the rise in oil prices associated with the bombings of Iran — even if temporary — tends to make the currently expected reduction in the policy rate much less likely. Evidence of persistent inflationary pressures was already emerging due to labor cost dynamics and the interruption of the oil price decline cycle that had been in place since 2023. Added to these factors now is the possibility of an increase in costs associated with fuels and other petroleum-derived products. Even if not very persistent, it would definitely challenge inflation convergence to the target. |

- Financial markets reacted to the conflict in the Persian Gulf during the first few days largely as one would expect: 1) Without very meaningful adjustments, suggesting that markets are pricing in a short conflict with only temporary disruptions to oil supply and demand. 2) With virtually no impact on expected growth and only a small effect on projected inflation. 3) With a postponement — but not elimination — of expected further interest rate cuts by the Fed.

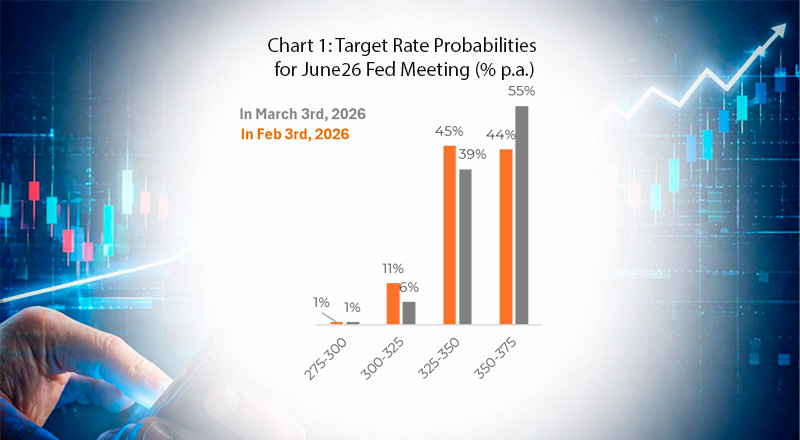

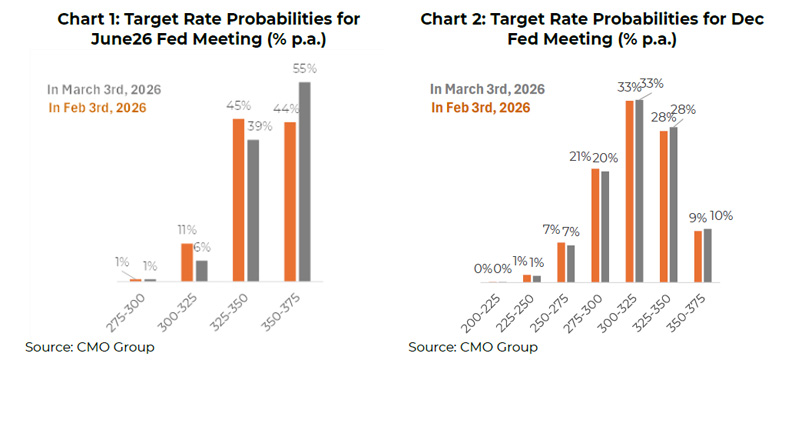

- According to estimates from the CME Group, one of the world’s largest derivatives exchanges, the most likely scenario for the Fed’s June decision has shifted from a 57% probability associated with a lower rate than the current one to a 55% implied probability of stability (Chart 1). For December, pricing still indicates around a 60% probability of one or two 25-basis-point cuts (Chart 2).

- This means that investors believed — and continue to believe — in the convergence of core personal consumption expenditures (PCE) inflation from 3% (in January) to at least 2.5% by the end of the year. Much of this belief may stem from the fact that the core measure excludes not only food but also energy prices. Nevertheless, the potential magnitude and persistence of cost pass-through along the supply chain — the so-called second-round effects — should not be underestimated.

We have argued that the scenario of inflation converging to target was already proving challenging even before the conflict in the Middle East, a situation that is now likely to worsen. We had highlighted the impact of higher import tariffs, the expected disappearance of gasoline deflation, and the persistence of price increases in the services sector. Even if temporary, the current shock is likely to aggravate the situation.

Pre-Existing Inflation Risks Associated with Wholesale Inflation

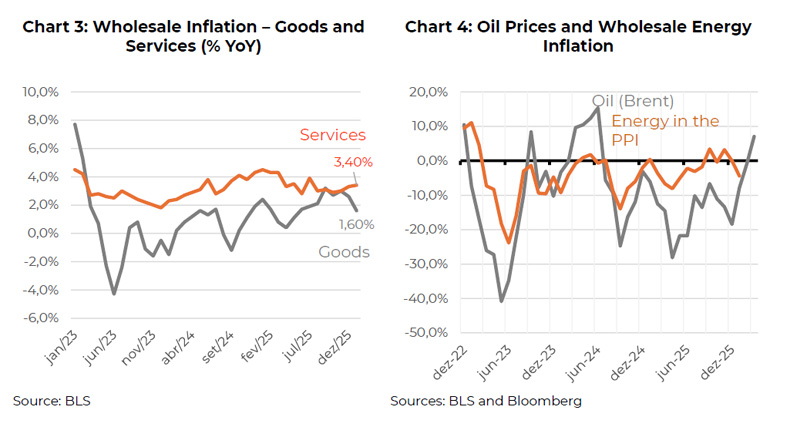

We have been drawing attention to the fact that inflation was already facing difficulties in converging to target even before the attacks on Iran. The most recent reading of wholesale prices had already surprised to the upside, largely due to the persistence of pressures associated with services provided to businesses (Chart 3). The current situation appears even more challenging as we are likely to lose the benefit of energy price deflation, which had prevailed for most of the past three years (Chart 4).

Although the direct impact of rising oil prices on core inflation measures may not appear significant — since energy items are excluded from their calculation — it should not be underestimated. First, we know that companies will attempt to pass higher transportation costs along the supply chain. The extent of this pass-through will depend largely on demand conditions, which still appear relatively strong.

In addition, oil prices will ultimately affect not only gasoline but also a wide range of petroleum-derived products, such as plastics and fibers. At the consumer level, price pressures may be felt in products such as plastic bags, PET bottles, containers, food packaging, household utensils, certain cosmetic products (such as creams and shampoos), pharmaceuticals, cleaning products (detergents, disinfectants), and clothing items that use nylon, polyester, and elastane.

For companies, the impact may be even greater, affecting inputs such as fertilizers, agricultural chemicals, solvents, plastic casings, cables, PVC, foams, paints, varnishes, plastics, and other synthetic materials.

Pre-Existing Inflation Risks Related to Consumer Prices

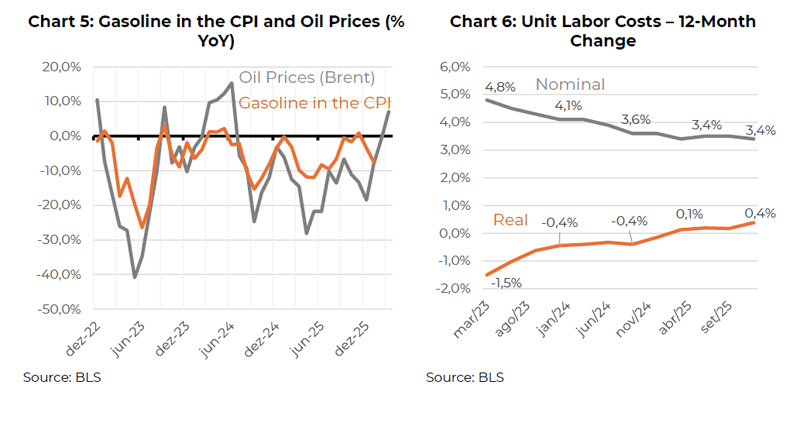

From the consumer side, the situation is no less challenging. Considering that gasoline carries a weight of roughly 4% in the headline CPI, the simple disappearance of the 7.5% deflation recorded in the 12 months through January 2025 would add 0.3 percentage points to the cost of living for households. Families would naturally attempt to offset this loss of purchasing power through higher wage demands. The relationship between oil prices and gasoline prices for consumers is shown in Chart 5. The fact is that gasoline prices are unlikely to remain stable and are quite likely to increase immediately.

The Employment Cost Index (ECI) measures the change over time in the hourly labor cost to employers. The ECI uses a fixed basket of labor to estimate cost changes, eliminating the effects of workers shifting across occupations and industries, and includes both wages and salaries as well as the cost of benefits.

Chart 6 shows the 12-month variations in labor costs, both in nominal and real terms. It is possible to observe the persistence of increases close to 3.5% per year, even in an environment of declining inflation. This implies increasingly larger real gains in employee compensation and rising labor costs for companies.

This dynamic reinforces the challenging outlook for inflation over the course of the year, now further aggravated by an oil shock whose magnitude and persistence remain uncertain.